Yes, you can challenge the value of your totaled car. In Oregon, your policy likely gives you a formal way to do it through the appraisal clause, and if the final appraised value comes in above the insurer's last offer, the insurer must reimburse reasonable appraisal costs.

That matters because many individuals ask the question only after they've opened the valuation report, seen a number that doesn't match the actual market, and felt boxed in. You're trying to replace a vehicle in a tight regional market, and the insurance company is acting like its first number is final. It isn't.

I work in this space from the policyholder side, and the pattern is familiar. The adjuster sends a CCC ONE or Mitchell report. The report looks official. The comparable vehicles aren't really comparable. The trim is off, the condition deductions are questionable, the market area is too broad, and the offer comes in short of what it would take to buy the same kind of vehicle in Oregon or Washington.

If you're asking, “Can I challenge the value of my totaled car?” the practical answer is yes, but you need to do it the right way. Complaining won't move the number. Evidence, procedure, and timing will.

Table of Contents

- Your Rights After a Total Loss Declaration

- Decoding the Insurer's Valuation Report

- Building Your Counter-Case with Real Evidence

- How to Formally Invoke the Appraisal Clause

- Navigating Negotiation Timelines and Costs

- Taking Control to Secure Your Fair Settlement

Your Rights After a Total Loss Declaration

The call usually goes the same way. Your adjuster says the car is totaled, gives you a dollar figure, and wants a quick answer. If you drive in Oregon or Washington, that first number often comes from a valuation system built to process claims efficiently, not to argue for every dollar your vehicle commands in the local market.

You do not have to accept the first total loss offer. In Oregon, policyholders can challenge a disputed value through the appraisal process described in the state's guidance on totaled vehicle claims and appraisal rights. If you want a local overview of how that process plays out, this guide to Oregon total loss appraisal disputes gives useful background.

What actual cash value really means

The insurer owes actual cash value, or ACV. That is the market value of your vehicle immediately before the crash. It is not your loan balance, your original purchase price, or the cost to buy a newer replacement.

On paper, that sounds straightforward. In a real claim, ACV disputes usually come from the inputs. A CCC ONE or Mitchell report can look polished and still miss the trim level, understate condition, ignore recent tires, or pull comparables from the wrong part of the region. Around Portland, Eugene, Bend, Vancouver, or Seattle, those mistakes can shift value fast because asking prices and dealer inventory vary a lot by metro area.

One point policyholders in Oregon often miss is the tax treatment. Oregon has no sales tax, so a fair settlement fight usually turns on the vehicle value itself, not on padding the claim with a sales-tax argument you might see in other states. That puts more pressure on getting the base valuation right the first time.

Practical rule: Treat the first ACV report like an estimate to audit, not a final answer.

Where your leverage comes from

Your policy gives the insurer a process, but it also gives you one. In a value dispute, the pressure point is usually the appraisal clause.

That clause changes the conversation from informal back-and-forth with an adjuster to a defined procedure. You pick an appraiser. The insurer picks one. If they cannot agree, an umpire decides the remaining gap. In Oregon and Washington, that matters for a simple reason. Carriers know many owners will argue by phone for a week, then give up. Far fewer owners put the dispute into appraisal with organized market data and someone who knows how total loss reports are built.

That is why the clause has real financial weight. It forces the insurer to spend money and defend its number inside a formal process instead of relying on claimant fatigue.

Oregon also gives policyholders an added advantage. As noted earlier in the state guidance, if the final appraised value comes in above the insurer's last offer, the insurer may have to reimburse reasonable appraisal costs. That reimbursement point is significant; it means a strong challenge can make financial sense, not just provide emotional satisfaction.

Decoding the Insurer's Valuation Report

Most major carriers use outside valuation systems. The names you'll see most often are CCC ONE, Mitchell, and Audatex. Those systems are common, but they are not infallible. A published review of total loss valuation disputes notes that these systems often undervalue vehicles by using out-of-area comparables, incorrect condition adjustments, or by missing custom parts and trim details, with settlements in many markets coming in 15–25% below fair market value according to this analysis of total loss valuation methods.

That doesn't mean every report is wrong. It means you should read it like an appraiser would.

If you're dealing specifically with a CCC report, this walkthrough on how to dispute a CCC ONE valuation report in Oregon can help you follow the line items.

The report is only as good as its inputs

The first place I look is the vehicle description. Year, make, model, trim, drivetrain, mileage, packages, wheels, upholstery, towing equipment, factory options, and major upgrades all need to be correct. One trim-level error can drag the whole report down.

Then I look at the comparable vehicles. Many reports appear polished until you inspect where those vehicles came from and what they are. A truck listed far outside your realistic buying area may satisfy the software, but it may not reflect your market. The same goes for a base model used to value a better-equipped version of the same vehicle.

Red flags that deserve a challenge

A weak total loss report usually gives itself away in a few places:

- Out-of-area comparables: Vehicles sourced from markets that don't match where you would replace the car.

- Trim mismatch: A lower trim, missing package, or wrong engine used as a “comparable.”

- Condition deductions that feel automatic: Deductions for interior, paint, tires, or prior wear that aren't supported by clear evidence.

- Missing equipment: Tow packages, premium audio, upgraded wheels, diesel packages, suspension setups, and similar value-bearing details left out.

- Specialty blind spots: Older clean trucks, diesel pickups, motorcycles, classics, RVs, and unusual builds often fit poorly into automated templates.

If the report values your vehicle as if it were generic, start assuming the output is generic too.

What usually doesn't work

Calling the adjuster and saying, “Your number is way too low,” won't do much. Neither will sending a screenshot of a Kelley Blue Book page and expecting the matter to resolve itself.

What does work is identifying exact report defects and replacing them with better evidence. You need to show why a listed comparable is not comparable, why an adjustment is unsupported, or why the system missed a feature that changes value. The more specific you get, the harder it is for the insurer to hide behind software.

Building Your Counter-Case with Real Evidence

Once you know where the report is weak, your job is to build a cleaner valuation. Not a louder one. A cleaner one.

Generic pricing guides don't solve this problem well in the Pacific Northwest. Broad consumer advice often points people to Kelly Blue Book or national listings, but those approaches can miss state-specific market realities. A discussion of total loss valuation guidance notes that Oregon's lack of sales tax and Washington's higher fuel costs can materially affect ACV in ways standard insurer reports often miss, especially when they rely on broad averages rather than local market evidence, as discussed in this overview of totaled car value guidance.

Start with local comparable vehicles

Look for vehicles that are close to yours in:

- Year and generation: Don't mix body styles or mid-cycle redesigns.

- Trim and powertrain: A diesel truck is not interchangeable with a gas truck. A premium trim is not a base trim.

- Mileage band: Close mileage matters because insurers often hide aggressive mileage adjustments inside the report.

- Condition and use type: A former fleet vehicle, rough work truck, or stripped-down auction unit is not a good comp for a clean privately owned vehicle.

- Geography: Stay local enough that the listing reflects the market you would shop in.

Sources like dealer listings and major vehicle marketplaces can help, but the key is selection, not volume. Three well-matched local comps beat a stack of random listings.

If you need a professional valuation rather than a self-built package, an independent total loss appraiser can assemble a formal evidence set and challenge flawed report inputs.

Document what the report missed

Don't assume the adjuster knows what your vehicle had or how you maintained it. Put it in writing and attach proof where you can.

Use a file that includes:

- Recent maintenance records: Show that the vehicle wasn't neglected.

- Major repair invoices: Transmission work, suspension work, cooling system repairs, brake service, and similar items can support condition.

- Tire receipts: Newer quality tires affect replacement-market appeal.

- Photos taken before the loss: Interior, exterior, bed, tow setup, accessories, and odometer photos help.

- Option verification: Window sticker, build sheet, purchase paperwork, or manufacturer records.

- Aftermarket or specialty equipment: Only include items that are documented and market-relevant.

Sometimes supporting evidence comes from unusual places. For example, if title history, prior use, or ownership questions are muddy and affect whether a listed vehicle is a valid comparable, outside records work can help. In more complicated factual disputes, people sometimes use private detective services to verify vehicle history or ownership details that ordinary online searching won't resolve.

Insurer's Valuation vs. Your Evidence-Based Valuation

| Valuation Component | Typical Insurer's Approach (CCC ONE) | Your Stronger Counter-Evidence |

|---|---|---|

| Vehicle details | Pulls from database fields that may contain trim or option errors | VIN-based option confirmation, photos, purchase documents |

| Comparable sales | Broad market pull that may include weak geographic matches | Local listings with matching trim, mileage, drivetrain, and equipment |

| Condition adjustments | Template deductions that can be hard to trace | Maintenance records, pre-loss photos, repair invoices |

| Regional market factors | Generalized pricing logic | Oregon and Washington replacement-market evidence from actual local listings |

| Specialty value | Often under-recognized in diesel, enthusiast, or unusual vehicles | Niche-market listings and model-specific feature support |

A solid counter-case is organized, restrained, and specific. Angry emails don't add value. Correcting the record does.

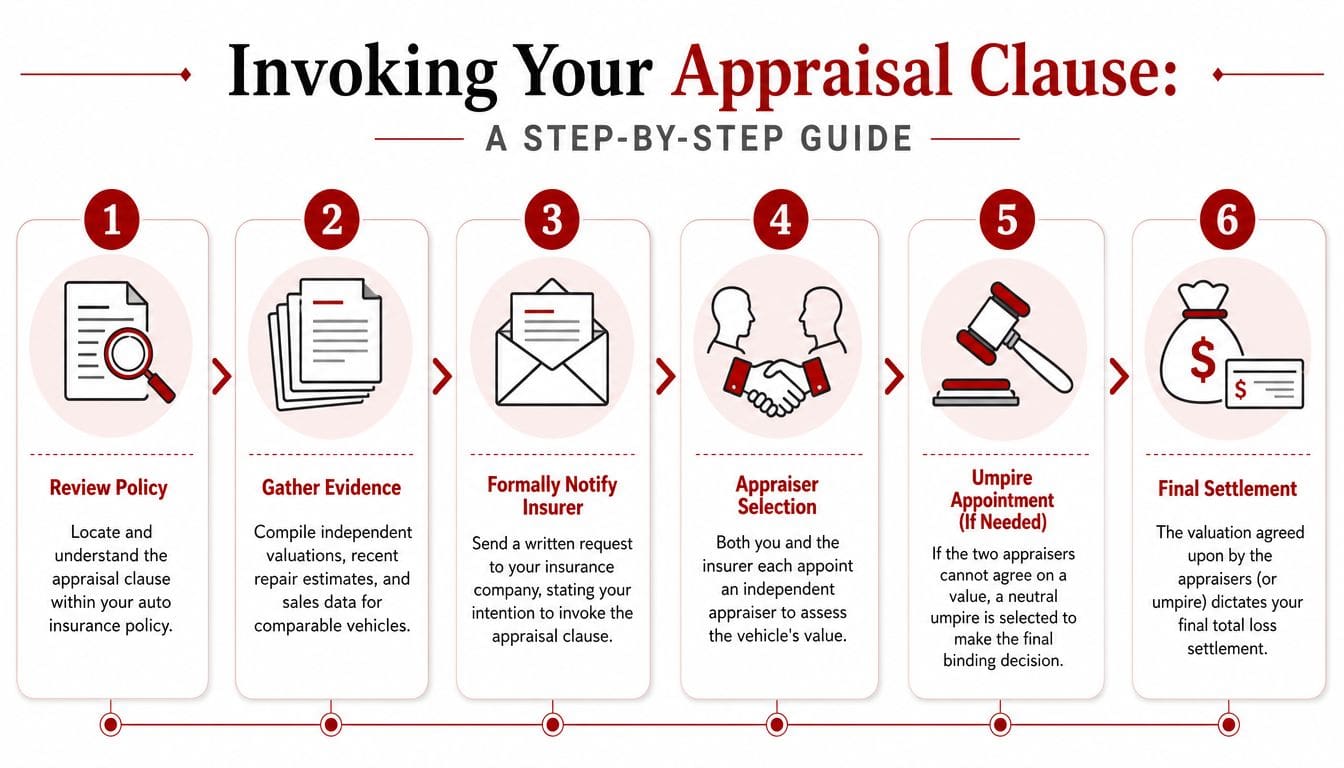

How to Formally Invoke the Appraisal Clause

Your adjuster sends a CCC ONE report, rejects your corrections, and tells you the number is final. That is usually the moment to stop debating by email and switch to the policy procedure that changes the incentives.

Once you invoke the appraisal clause, the claim moves out of the adjuster's discretion and into a defined dispute process. In Oregon, that matters for another reason noted earlier in this article. If the appraisal result comes in above the carrier's last offer, reimbursement of reasonable appraisal costs can become part of the discussion. In Washington, the pressure point is different. The clause still matters, but the cost and timing analysis can be less favorable if the value gap is small. That is why I tell owners in both states to decide based on dollars, not principle alone.

When to stop arguing and formalize the dispute

There is a right time to send the demand. Too early, and you have not built the record. Too late, and you waste days arguing with a valuation system that the desk adjuster is not going to abandon on their own.

A practical trigger is this: you have already identified the bad comparables, the trim or option errors, the unsupported condition deductions, and the local market mismatch, and the carrier still stands on the report. Around Portland, Eugene, Vancouver, Spokane, and the Puget Sound market, I also look at whether the report ignored local replacement realities. Oregon's lack of sales tax can affect what a real buyer would pay to replace the vehicle. That does not mean every Oregon car should be worth more. It means the local market needs to be analyzed correctly instead of pulled from a broad database spread.

Use this sequence:

- Read the appraisal clause in your policy and confirm it applies to disputes over value.

- Finish your evidence file first so your appraiser can start with a clean record.

- Send a written appraisal demand by email or another method you can document.

- Name your appraiser, or state that you will provide the name promptly if you are still finalizing it.

- Ask the carrier to identify its appraiser in writing and confirm that the claim is being transferred into appraisal.

The video below provides a walkthrough of the process.

Simple language you can use

Keep the notice short. This is not the place for a four page argument about every bad comparable in the CCC report.

I dispute your valuation of my total loss vehicle and hereby invoke the appraisal clause under my policy. Please confirm in writing that you accept this appraisal demand and provide the name and contact information for the insurer's selected appraiser. I will provide my appraiser's information and supporting valuation materials.

That wording works because it does three things. It states the dispute clearly, invokes the contract right clearly, and asks for a written response. Save the detailed valuation fight for the appraiser. Mixing everything into the demand letter often creates delay and gives the carrier more room to sidestep the actual invocation.

Choosing the right appraiser

This decision affects outcome more than the letter itself.

You want someone who handles total loss files for owners, understands how CCC ONE reports are built, and knows how Oregon and Washington markets differ in practice. A generic appraiser who mainly inspects repair damage may not be the right fit. Total loss appraisal is part valuation work, part document work, and part negotiation.

A company handling total loss appraisal clause disputes for policyholders in Oregon and Washington is an example of such a firm. Whether you hire that company or another one, ask direct questions before you sign anything:

- Who is their regular client base? Consumer work and carrier work are not the same practice.

- Do they audit CCC ONE reports line by line? That includes options, trim, condition adjustments, and comparable selection.

- Do they know the local replacement market? Oregon tax treatment, Washington border market effects, truck pricing, and AWD demand all matter in the Northwest.

- Will they negotiate the file after writing the report? Some appraisers produce a number and disappear.

- Have they handled your vehicle type before? Diesel pickups, Subarus, motorcycles, vans, classics, and modified vehicles each create different valuation problems.

One caution I give clients all the time. Do not invoke appraisal just to “send a message.” Invoke it when the likely gain is real and the file is strong. That is how you turn a bad total loss offer into a process the insurer has to take seriously.

Navigating Negotiation Timelines and Costs

Once both appraisers are named, the file usually becomes more technical and less emotional. That's a good thing.

Your appraiser reviews the insurer's report, builds a supportable market value, and negotiates directly with the carrier's appraiser. In strong files, that stage often resolves the dispute without further escalation. The insured usually hears less during this phase, which can feel strange, but that doesn't mean nothing is happening. It means the discussion has moved into the valuation lane where it belongs.

Who does what after the clause is invoked

Three people can shape the result:

- Your appraiser: Builds your value case, attacks bad comparables, supports proper ones, and negotiates.

- The insurer's appraiser: Defends the carrier's position, though some are more reasonable than others once the file is closely examined.

- The umpire: Steps in only if the two appraisers can't agree.

Most policyholders focus on the final number. Experienced people also focus on the path to that number, because costs can change whether a dispute was worth pursuing.

The umpire issue most people learn too late

The umpire stage carries a real financial risk. A published discussion of appraisal disputes notes that umpire fees are often $1,000 to $2,000, split between the parties, and that if the valuation gap is small, the cost can erase much of the benefit of pushing the case that far, as explained in this discussion of appraisal clause umpire costs.

That creates a break-even question. If the gap between your side and the insurer's side is narrow, escalation may win the technical dispute and still leave you with little practical gain.

The smartest appraisal strategy is not “force the umpire.” It's “build a file strong enough that the other side wants to settle before the umpire.”

When an attorney may make sense

A valuation dispute alone doesn't always require a lawyer. Many total loss disagreements are appraisal issues, not legal-liability issues.

An attorney may become useful when the case includes claim handling problems beyond value, such as coverage disputes, title issues, unreasonable delays, or broader accident-related damages. But if the core problem is that the total loss number is wrong, a capable independent appraiser is often the first call, not the last resort.

The main practical question is this: are you fighting about what the vehicle was worth, or are you fighting about something bigger than value? If it's value, stay disciplined and keep the process focused there.

Taking Control to Secure Your Fair Settlement

You open the CCC ONE report, see a number that will not buy your car back in Portland, Eugene, Vancouver, or Tacoma, and the adjuster acts like the file is finished. It is not finished. A total loss value is only as good as the comps, adjustments, and condition calls behind it.

The policyholder who does best in this stage usually stops treating the insurer's figure like a verdict and starts treating it like an opinion that has to be tested. In Oregon and Washington, that shift matters because the appraisal clause changes the pressure on both sides. Once you show that your file is organized, local, and defensible, the carrier has to decide whether it wants to spend more money defending a weak valuation.

That is the practical answer to the question here. Yes, you can challenge the value of your totaled car, and in the Pacific Northwest there is a clear process for doing it without drifting into pointless arguments with an adjuster who did not build the report.

I have seen the same pattern over and over with Oregon and Washington claims. The software pulls broad-market comparables, misses equipment, smooths over condition, and treats clean local vehicles as if they are interchangeable with average inventory from outside the area. Oregon adds another wrinkle. Buyers do not pay sales tax on vehicle purchases, so replacement pricing and dealer behavior do not always line up neatly with national assumptions built into valuation systems.

That does not mean every insurer valuation is wrong. It means you should ask a harder question. Can the number be supported by actual local market evidence once the bad comps, missing options, and questionable deductions are stripped out?

If the answer is no, push the claim in a disciplined way.

Use the report line by line. Challenge the comparables that do not match. Correct the trim, packages, mileage, prior damage assumptions, and condition calls. Put local dealer listings, recent regional sales, service history, photos, and ownership records in one file. If the carrier still holds to a weak number, the appraisal clause gives you a structured way to move the dispute out of adjuster back-and-forth and into a value process where each side has to put up real support.

That is where financial incentives start to matter. An insurer may be comfortable holding a low number when the policyholder is only objecting by phone or email. The calculation changes when the carrier sees that you understand the clause, have support from Oregon or Washington market data, and are prepared to make the company pay to defend its position.

A polished PDF is not proof. It is a starting point.

If you want an outside review before deciding whether to accept, negotiate, or invoke appraisal, Auto Appraisals provides Oregon- and Washington-focused total loss claim reviews, independent appraisals, and appraisal clause support for policyholders building a fair market value case.