You get the call. The adjuster says your vehicle is a total loss, then emails a valuation report that looks polished, official, and far too low. You scan the number once, then again, because it doesn't line up with what it would cost to replace your truck, SUV, car, RV, or specialty vehicle in your market.

That reaction is usually justified.

Most policyholders aren't upset because they “want extra money.” They're upset because the offer doesn't buy back what they lost. The hard part is that the insurer's report often looks technical enough to shut the conversation down. It cites CCC ONE, Mitchell, or J.D. Power. It includes adjustments, comparable vehicles, and condition deductions. To someone who doesn't work these files every week, it can feel final.

It isn't final. A low total loss offer is often the start of the dispute, not the end of it. An Independent Total Loss Appraiser doesn't just rerun software. A qualified appraiser tears apart weak comparable selections, corrects missing options and bad condition adjustments, replaces out-of-area listings with real local market evidence, and negotiates from a documented position the carrier has to answer.

Table of Contents

- Your Total Loss Offer Is Low Now What

- What an Independent Total Loss Appraiser Actually Does

- The Appraisal Clause Process From Start to Finish

- When to Hire an Independent Appraiser

- Choosing a Qualified Appraiser in Oregon and Washington

- Costs Timelines and Fee Reimbursement in Oregon

- Take Control of Your Total Loss Settlement

Your Total Loss Offer Is Low Now What

The usual sequence is predictable. Your vehicle is damaged, stolen, flooded, or hit by a tree or deer. Then the insurer declares it a total loss and sends a number that feels disconnected from your real replacement cost. You call, explain that the offer is too low, and get a version of the same answer: “That's what the report supports.”

That's the moment many people make their biggest mistake. They argue from frustration instead of evidence.

If your vehicle was a diesel truck, a clean older SUV, a well-kept specialty car, or something harder to match, the gap can feel even worse. The insurer may have used comparables from the wrong area, ignored equipment, or applied deductions that don't reflect the vehicle's actual pre-loss condition. If you're also dealing with larger equipment or coach-style units, the documentation issues can overlap with the same headaches people face when handling RV insurance claims.

You are not required to treat the insurer's first offer as the true market value of your vehicle.

The practical move is to slow down and get the valuation report reviewed before you sign anything. If you're trying to understand your options for pushing back, a focused guide on how to challenge a total loss offer is a good place to start.

What changes once you stop reacting and start disputing

A total loss dispute becomes manageable when you reframe it correctly:

- The first offer is a position, not a verdict. Carriers start with a valuation they believe they can support. That doesn't mean it's accurate.

- The report can be audited. Trim, mileage, options, condition, and comparable location all affect value.

- Your policy may give you a formal path. That path is usually the appraisal clause.

- An Independent Total Loss Appraiser works your side of the file. The job is to document a supported value and negotiate it through the policy process.

Most frustration comes from not knowing what to do next. Once you know the dispute has a structure, the situation changes. You stop trying to win an argument on the phone and start building a case.

What an Independent Total Loss Appraiser Actually Does

You receive the insurer's valuation, glance at the number, and know it does not match the vehicle you owned. Same year, same make, same model on paper. Wrong trim. Missing packages. Comparables from outside your market. Condition deductions with no support. That is the point where an independent appraiser earns their fee.

Independence matters more than people think

In total loss work, independence is about who the appraiser answers to and how the file gets built. Your appraiser should work for you alone, outside the carrier's vendor network and outside the valuation platform being challenged.

That matters because the job is to audit the insurer's number against the policy standard for market value, then support a different number if the report falls short. A good appraiser is not there to move paperwork along. They are there to examine the valuation line by line, document the defects, and present a supportable replacement.

For policyholders who want context on how write-off terminology differs in other markets, this guide for motor traders on write-offs is useful background.

The critical work happens inside the valuation report

A lot of people assume an independent appraiser just runs another software report and hopes for a better result. That is not how serious total loss work gets done. The value comes from correcting bad inputs, checking whether the insurer used comparable vehicles that belong in your market, and making judgment calls that software cannot make well.

Here's what that work looks like on a file:

| Problem in insurer report | What an independent appraiser checks | Why it changes value |

|---|---|---|

| Wrong trim or configuration | VIN decode, factory build data, model details | One trim level down can pull the whole valuation lower |

| Missing options or packages | Factory and installed equipment review | Features that affect sale price need to be counted |

| Poor comparable selection | Local dealer listings and market comparison review | Out-of-area comps can understate replacement cost in your area |

| Bad condition deductions | Pre-loss photos, service history, ownership records | Unsupported deductions reduce value without proof |

| Generic treatment of specialty vehicles | Segment-specific market analysis | Diesel trucks, classics, motorcycles, and RVs need category knowledge |

The manual review is where claims turn. I have seen reports miss towing packages, premium audio, off-road packages, and trim upgrades that matter in the market. I have also seen “comparable” vehicles pulled from areas where pricing is materially lower, then adjusted in a way that still leaves the insured short.

That work cannot be delegated to CCC ONE or any other valuation system and treated as finished. Software can organize listings and apply formulas. It cannot inspect whether the source data is wrong, whether the condition adjustment is defensible, or whether a local buyer would treat two vehicles as true substitutes.

Negotiation is the other half of the assignment. A corrected report still has to be presented by someone who understands how carriers defend their numbers, which points are strongest, and where weak adjustments can be forced off the table. That is why a skilled appraiser often improves the settlement. The gain comes from better facts, better comps, and better advocacy inside the appraisal process.

Practical rule: If the insurer's valuation does not hold up under line-by-line review, the settlement figure usually does not hold up either.

If you want to see the workflow in a service context, total loss appraisal services typically involve reviewing the insurer report, correcting the valuation evidence, and presenting a supported market value for negotiation.

The Appraisal Clause Process From Start to Finish

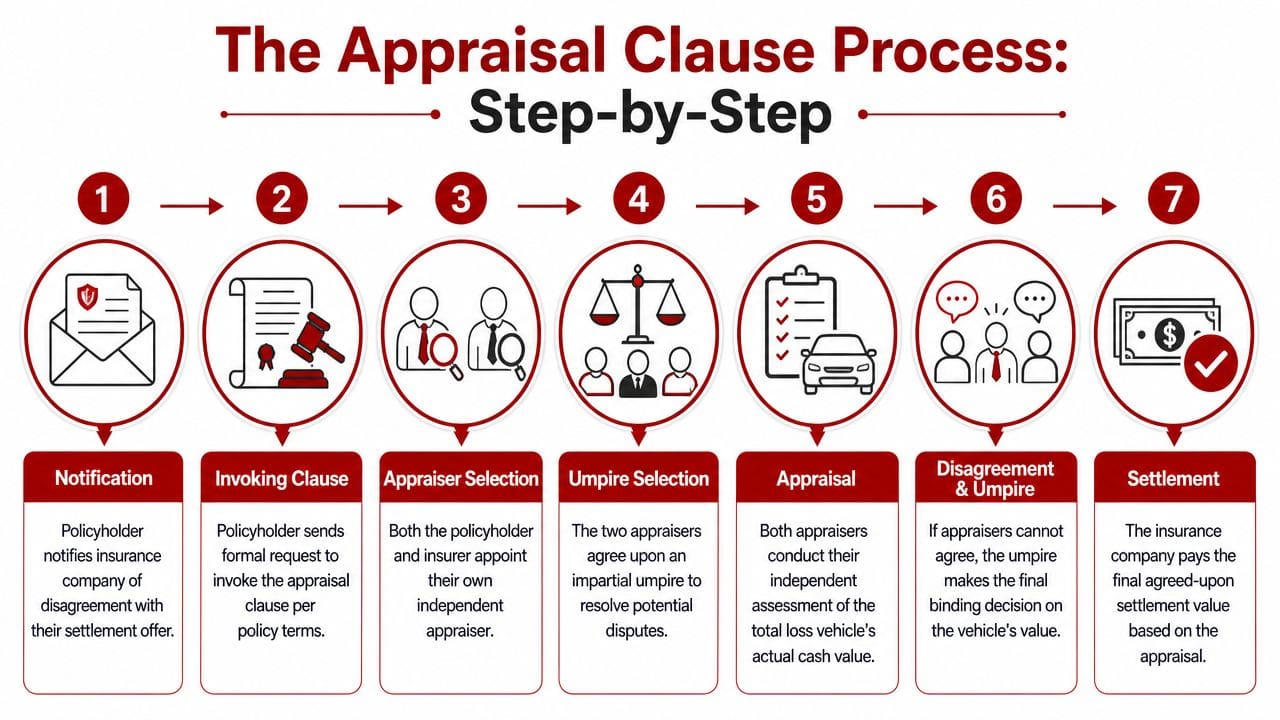

Hearing “appraisal clause” often leads to the assumption that the process is complex, expensive, or close to litigation. It usually isn't. It is a structured valuation dispute mechanism built into many auto policies.

A visual overview helps first.

How the dispute usually begins

You review the insurer's offer and determine there's a value dispute. Then you or your appraiser send written notice invoking the appraisal clause under the policy language. The key is that this process addresses value, not broader coverage or liability disputes.

The insurer then appoints its appraiser. You appoint yours. In Oregon, if you're dealing with a total loss dispute under the appraisal clause, the legal framework is important enough that many policyholders benefit from reading a state-specific explanation of Oregon total loss disputes.

A simple sequence looks like this:

- You reject the valuation amount.

- You invoke the appraisal clause in writing.

- Each side names an appraiser.

- The appraisers exchange evidence and attempt to agree.

- If they cannot agree, they select an umpire.

- Any agreement between two of the three resolves the value dispute.

- The insurer pays based on that result, subject to policy terms.

What happens between the two appraisers

This is the part policyholders rarely see, but it's where the result is usually shaped.

Your appraiser audits the insurer's report, documents errors, builds a competing valuation, and supports it with market evidence. The insurer's appraiser defends the carrier position or revises it if the evidence warrants movement. The quality of that exchange matters more than is often realized.

A weak appraiser sends a number. A strong appraiser sends a case file.

That file may include:

- Comparable vehicle corrections tied to your local market

- Option verification when the carrier report missed equipment

- Condition rebuttals supported by photos or maintenance records

- Specialty valuation logic for trucks, classics, motorcycles, or RVs

- Negotiation analysis that explains why certain comps should be excluded or adjusted

Later in the process, it often helps to hear a plain-language walkthrough before documents start moving. This video gives that kind of overview:

When an umpire enters the process

Often, attention fixates on the umpire. In reality, the strongest cases are often resolved before it gets that far because one side's evidence becomes difficult to defend.

If the two appraisers still can't agree, they select a neutral umpire. The umpire reviews the competing positions and decides the unresolved value questions. That decision is binding within the appraisal framework.

The process works best when the policyholder's side presents a disciplined valuation package, not a list of online ads and a demand.

The biggest practical point is this: invoking appraisal changes the dispute from a casual back-and-forth with an adjuster into a formal evidence-driven process. That alone often changes the tone of the claim.

When to Hire an Independent Appraiser

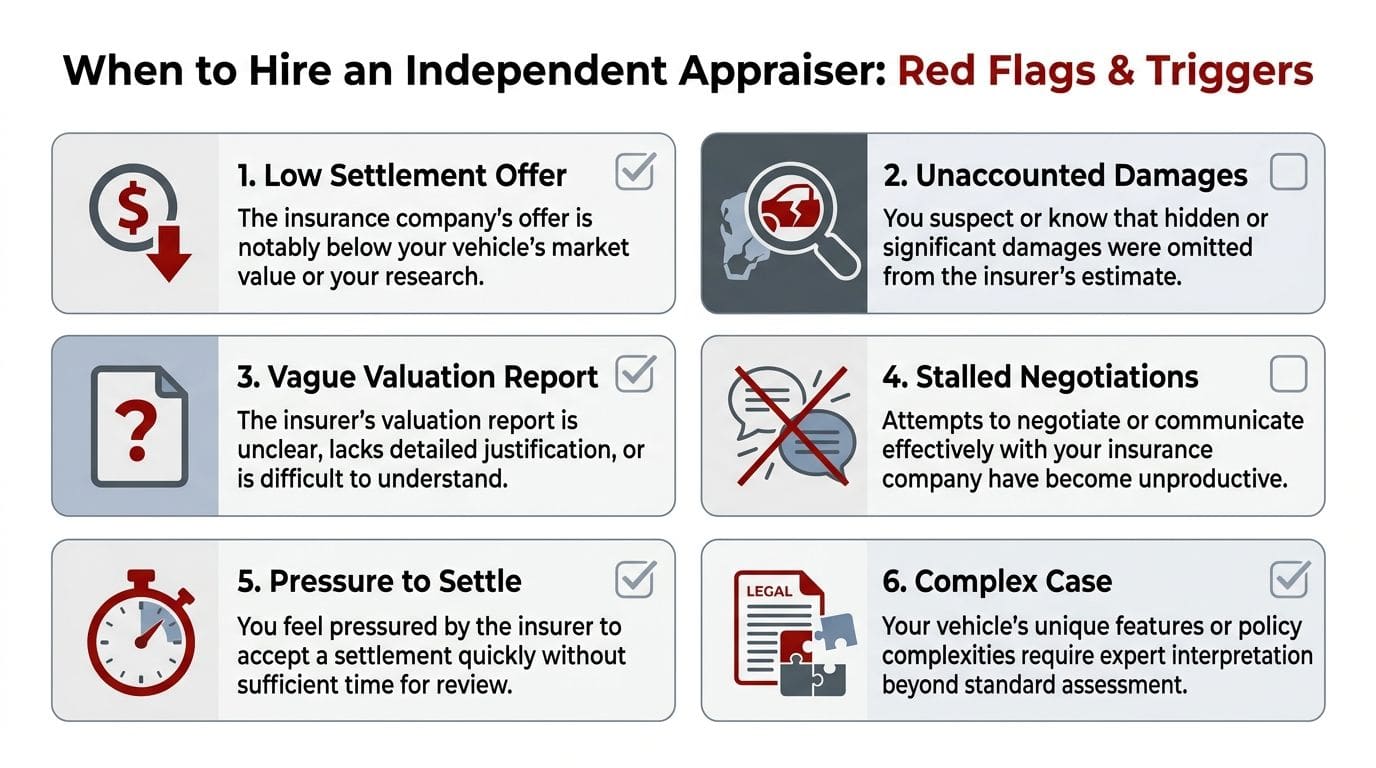

Some disputes don't need outside help. Many do. The difference usually comes down to whether the insurer's valuation contains errors you can identify and prove, and whether the vehicle is simple enough for the market data to be clean.

Red flags inside the insurer report

If you see any of these, the file deserves a serious review:

- Comparable vehicles are from the wrong market. A report built on listings from a distant city can distort replacement value.

- The trim level is wrong. This is one of the fastest ways to suppress a valuation.

- Options are missing. Tow packages, premium trim features, drivetrain details, and major equipment matter.

- Condition deductions look inflated. If the report marks your vehicle down without real support, that's worth challenging.

- The report is hard to follow. Confusing reports often hide weak assumptions in the adjustments.

These aren't technicalities. They are value drivers.

Cases where software often misses the mark

Automated reports tend to struggle most when the vehicle isn't a basic, common commuter car in a perfectly documented segment.

That includes:

- Diesel trucks where engine, drivetrain, trim, and local demand can materially affect value

- Classics and collector vehicles that need judgment, not just database output

- Modified 4x4s and specialty builds where equipment matters

- Motorcycles and RVs with configuration differences generic systems don't handle well

- Exceptionally clean older vehicles that are worth more than average-condition examples

In those files, a professional review isn't about being combative. It's about preventing a generic valuation tool from flattening the actual market story of your vehicle.

A practical way to think about it is simple. If the insurer's report looks close and the vehicle is straightforward, you may only need a review. If the report has multiple errors, negotiations have stalled, or the vehicle is specialized, hiring an appraiser usually makes sense much earlier.

Choosing a Qualified Appraiser in Oregon and Washington

Not every appraiser who advertises total loss help is legally qualified to handle an appraisal clause dispute in Oregon. That distinction matters.

What Oregon requires

In Oregon, the appraisal clause process has a specific legal requirement. Under ORS 742.466, any independent appraisal must be performed by a person holding a certified vehicle appraiser certificate under ORS 819.480, and only certified professionals can legally represent a policyholder in that total loss dispute process, according to Johnson Law's discussion of the Oregon appraisal clause.

That requirement screens out a lot of people who may sound knowledgeable but are not qualified to perform the appraisal clause role. A body shop, sales consultant, unlicensed consultant, or generic “claims expert” is not a substitute for a properly certified Oregon vehicle appraiser.

How to vet real independence

Once legal qualification is clear, the next question is conflict.

Ask direct questions:

| What to ask | Why it matters |

|---|---|

| Do you ever work for insurers or insurer vendors? | You want consumer-only representation if independence is the goal |

| Do you handle appraisal clause disputes or only provide reports? | Some providers stop at the report and don't negotiate |

| Do you know the local Oregon or Washington market? | Local comparable selection is central to value |

| Have you handled specialty vehicles like diesel trucks, classics, motorcycles, or RVs? | Segment knowledge changes the quality of the valuation |

| Who works the file? | Senior involvement matters in negotiation-heavy claims |

If you're comparing options, focus less on polished marketing and more on process. Ask how the appraiser handles CCC ONE, Mitchell, or J.D. Power reports. Ask how they document condition disputes. Ask whether they personally negotiate with the opposing appraiser or pass the file around.

An appraiser who works exclusively for policyholders brings a cleaner perspective to the dispute. That includes Oregon-based firms such as a company specializing in auto appraisals, which handle appraisal clause disputes and total loss negotiations for vehicle owners in Oregon and Washington.

A qualified appraiser should be able to explain exactly how they challenge a low valuation, not just promise a better result.

Washington policyholders should still ask the same practical questions even though the legal structure and reimbursement treatment can differ from Oregon. Licensing, independence, market knowledge, and negotiation skill still matter.

Costs Timelines and Fee Reimbursement in Oregon

The first question many people ask is the right one: what will this cost me, and am I taking a financial risk by disputing the offer?

What you're really paying for

You are not paying for “another opinion” in the casual sense. You're paying for professional valuation analysis, document review, market research, claim strategy, and negotiation inside a policy-based dispute process.

That can include:

- Report analysis of CCC ONE, Mitchell, or J.D. Power valuation materials

- Comparable research focused on relevant local market listings

- Condition and equipment review using records and documentation

- Formal appraisal work tied to the appraisal clause

- Negotiation with the insurer's appraiser

- Umpire coordination if needed

The exact fee model varies by provider and by case complexity. What matters in Oregon is that the law can change the financial exposure significantly.

What Oregon law does for policyholders

Under OAR 836-080-0240, if the final appraised value of a totaled vehicle exceeds the insurer's last offer, the insurer must reimburse the policyholder for all reasonable appraisal costs, as explained in this overview of Oregon total loss appraisal reimbursement rules.

That has a major practical effect. In many successful Oregon disputes, the appraisal process is effectively free to the consumer at the end because the insurer has to reimburse those reasonable costs.

A related Oregon consumer protection point is also unusually strong. Under ORS 742.466, if a certified vehicle appraiser determines a value higher than the insurer's last offer, even by one cent, the insurer must reimburse the policyholder's appraisal costs, and the same Oregon-specific framework is described in this explanation of Oregon total loss law. That source also states that independent appraisers help clients increase total loss settlements by up to 30% compared to initial insurer offers in documented scenarios.

For Oregon policyholders, that changes the decision. It's not a case of weighing a service fee against a possible better number. You may be using a legal process designed to let you challenge an undervaluation without carrying the long-term cost yourself if the appraised value beats the insurer's offer.

How long the process usually feels

Timelines vary with the quality of the carrier response, the complexity of the vehicle, and whether an umpire is needed. A straightforward file moves faster than a specialty vehicle dispute with heavy comparable disagreement.

Instead of focusing on a fixed number of days, focus on these practical timing factors:

- How quickly you invoke the clause

- How fast each side names an appraiser

- Whether records, photos, and equipment details are available

- How far apart the two valuations are

- Whether umpire involvement becomes necessary

Bottom line: In Oregon, the reimbursement rules remove much of the fear that keeps policyholders from challenging a weak total loss offer.

The biggest delay usually comes from waiting too long to act. Once the dispute is formalized and the evidence package is built, the process becomes much more predictable.

Take Control of Your Total Loss Settlement

A low total loss offer feels personal because the consequences are personal. You still need transportation. You still have to replace what was lost. And the report sitting in your inbox often looks more authoritative than it deserves.

The important shift is this: your dispute does not rise or fall on how frustrated you are. It rises or falls on evidence.

A capable Independent Total Loss Appraiser changes the claim by doing work software doesn't do well on its own. That means correcting bad comparable choices, identifying missing equipment, challenging unsupported condition deductions, using local market data that fits your vehicle, and negotiating inside the appraisal clause process with someone who knows how these files are defended.

If you're in Oregon, state law gives you a stronger position than many policyholders realize. If your appraised value comes in above the insurer's last offer under the applicable Oregon rules discussed above, reimbursement of reasonable appraisal costs can make the process far less risky than people assume.

You do not need to accept a low number just because it arrived in a formal-looking report. You need to know whether that report is right.

If you want a second set of eyes on your claim, Leverage Auto Appraisals offers no-obligation total loss claim reviews for Oregon and Washington policyholders. A review can tell you whether the insurer's report looks supportable, where the weak points are, and whether invoking the appraisal clause makes sense for your situation.