You just got the total loss call. The adjuster gave you a number, and within a few seconds you knew it was wrong. It won't buy the same vehicle in your local market. It doesn't reflect the condition your car was in before the loss. And the valuation report looks technical enough that it can make one feel pushed into accepting it.

That reaction is normal. A low total loss offer feels final because the insurer presents it that way. It isn't final.

In Oregon and Washington, owners have more advantage than most realize. The key is knowing where the insurer's report is vulnerable, how to build a replacement-grade valuation, and when to stop arguing with the adjuster and shift the dispute into a formal appraisal process. That's how you challenge a total loss offer effectively. Not with emotion, but with better market evidence and the right procedure.

Table of Contents

- That Sinking Feeling A Lowball Total Loss Offer

- Deconstructing the Insurers Valuation Report

- Building Your Evidence Based Counter Offer

- Invoking the Appraisal Clause Your Strongest Move

- Navigating the Appraisal and Negotiation Process

- Escalation Strategies Umpire and Legal Options

That Sinking Feeling A Lowball Total Loss Offer

The pattern is familiar. A vehicle owner gets rear-ended, hit by a deer, or comes out after a wind event to find major damage. A few days later the insurer says the car is a total loss and gives an offer that sounds clean and efficient. Then the owner starts shopping for replacements and realizes the number doesn't come close.

That gap is where most frustration starts. You know what you had. The insurer knows what its software says. Those are not the same thing.

I've seen owners talk themselves out of pushing back because the report looks official. CCC ONE, Mitchell, condition adjustments, comparable vehicles, option packages. It all looks settled. But the first total loss number is still an offer. It is not a judge's ruling, and it is not the only value that can be supported.

Most low total loss disputes don't turn on a dramatic mistake. They turn on a stack of small valuation errors that all lean in the insurer's favor.

If English isn't your first language, or if your policy language feels dense, get help before you respond. A practical resource for that is Translators USA policy translation solutions, especially when you need to understand the appraisal clause and settlement language before signing anything.

The most important shift is mental. Stop treating the adjuster's number like a fixed fact. Start treating it like a position you can test. If you're dealing with an Oregon total loss, review the legal and procedural basics first through this guide on Oregon total loss disputes.

Why owners lose leverage too early

Owners usually lose ground in three ways:

- They accept the first report at face value. They assume the comparable vehicles must be correct because a software system produced them.

- They argue conclusion instead of evidence. Saying “my car was worth more” won't move a file. Showing trim-specific, local, like-kind comparables might.

- They wait too long to invoke the policy process. Once informal back-and-forth stalls, continuing to repeat the same points rarely helps.

Washington owners face many of the same practical problems. Even when policy language differs, the playbook is similar. Read the report closely, identify the errors, build your market file, and use the appraisal clause when the insurer won't correct the valuation voluntarily.

Deconstructing the Insurers Valuation Report

Most total loss reports are built to look objective. They use defined terms, charts, line-item adjustments, and comparable vehicle grids. That presentation can hide the actual issue. The insurer's number is only as reliable as the inputs.

What the report is really trying to do

The insurer is trying to estimate Actual Cash Value, usually shortened to ACV. In plain language, that means the vehicle's market value immediately before the loss. The report tries to reach that number by selecting comparable vehicles and then adjusting for differences in mileage, equipment, condition, and prior damage.

That sounds reasonable. The problem is execution.

A bad total loss report often uses “comps” that aren't comparable. It may rate your vehicle's condition too harshly. It may miss factory packages, trim details, or equipment that matter in the retail market. Those mistakes don't always look dramatic one by one. Together, they can drag the value down enough to change the settlement materially.

In Oregon, there's another issue owners need to understand. The statutory threshold for declaring a vehicle a total loss is if repair costs equal or exceed 80% of the vehicle's Actual Cash Value, and that 80% rule is a legal benchmark, not just a guideline, as discussed in Oregon's total loss threshold overview.

Where the weak points usually are

The first place I look is the comparable vehicle list. If the report uses vehicles from outside the local market, the file may be vulnerable immediately. A market valuation only works when the market matches where you would have shopped.

The second place is condition. Insurers often apply condition deductions in a way that treats normal ownership wear like a premium defect. Minor seat wear, small chips, or age-appropriate use can get translated into valuation penalties that don't reflect what buyers discount in the local retail market.

The third place is equipment and trim accuracy. A wrong engine, wrong drivetrain, wrong package, or missed premium option can distort the entire comparison set.

Use this review lens:

| Report area | What to check | Why it matters |

|---|---|---|

| Comparable vehicles | Locality, trim, drivetrain, mileage spread | A weak comp set produces a weak ACV |

| Condition adjustments | Whether deductions reflect real pre-loss condition | Overstated deductions suppress value |

| Options and packages | Factory and aftermarket features | Missing equipment can understate replacement value |

| Prior damage notes | Whether prior damage is documented or assumed | Unsupported deductions should be challenged |

Practical rule: If the report cannot explain why each comp is genuinely like-kind to your vehicle, it is not a report you should accept without challenge.

If your report came from CCC ONE and you want a breakdown of the common failure points, this resource on how to dispute a CCC ONE valuation report in Oregon walks through what to examine line by line.

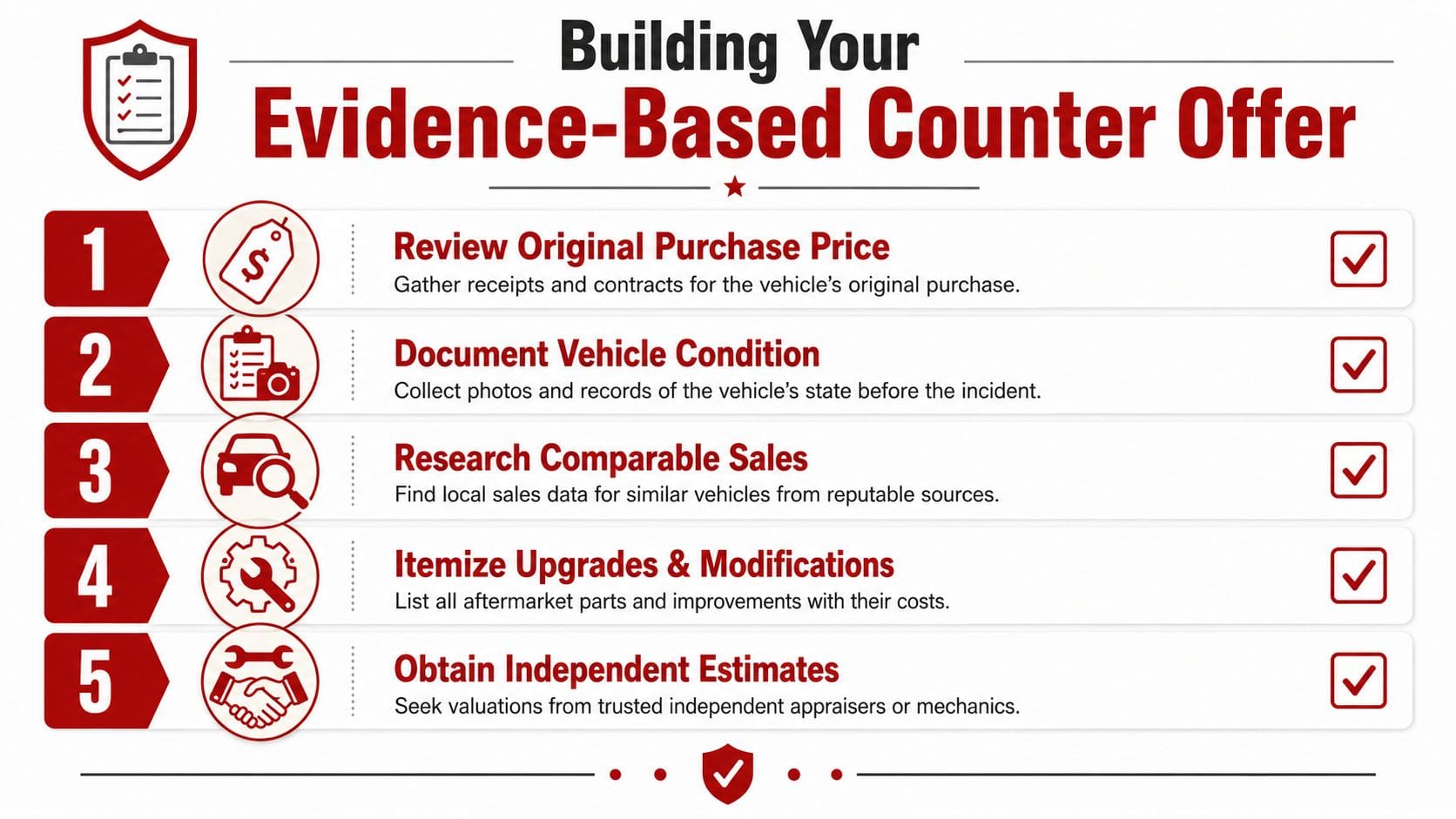

Building Your Evidence Based Counter Offer

A successful challenge total loss offer file is built, not improvised. The owners who get traction are the ones who stop debating and start documenting.

Start with your own vehicle file

Before you look outward at the market, lock down the facts about your vehicle. You need a clean record of what the vehicle was, how it was equipped, and what condition it was in before the loss.

Gather these first:

- Service history: Maintenance records help support that the vehicle was cared for and not neglected.

- Recent repair receipts: Tires, brakes, major service, suspension work, batteries, and similar items matter because they affect real-world retail appeal.

- Photographs: Use pre-loss photos if you have them. If not, use any recent images that show body condition, interior condition, wheels, accessories, and odometer.

- Build details: VIN-based equipment, trim package, drivetrain, cab or body configuration, towing packages, technology packages, and specialty features.

This is especially important for trucks, diesel vehicles, RVs, motorcycles, and specialty builds. Those files often fail because the insurer's software flattens real differences that buyers pay attention to.

A valuation model can also miss regional pricing factors. Insurers often rely on automated valuation models like CCC ONE that use non-local, flawed comparable vehicles, ignoring regional dynamics like Oregon's no-sales-tax advantage, which can artificially depress a vehicle's value by thousands, as noted in this discussion of automated valuation model problems and total loss negotiations.

Here's a quick explainer that helps many owners understand the process before they reply to the adjuster:

Build local comparables that actually match

Here, most do-it-yourself disputes either get strong or fall apart.

Don't just pull the cheapest vehicles you can find online. And don't rely on broad pricing guides as your primary proof. You need retail listings for vehicles that are close to yours in the ways that drive value.

Look for:

- Same trim level: An XLT is not the same as a Lariat. A base model is not the same as a premium package vehicle.

- Same engine and drivetrain: This is critical on trucks and SUVs.

- Close mileage band: A large mileage gap makes the comparison weaker.

- Same body style and configuration: Cab type, bed length, AWD versus FWD, seating layout, and similar features matter.

- Reasonably local market: If a buyer in your area wouldn't realistically shop there, the comp may not reflect your market.

A strong comp answers one question clearly: “If I had to replace this vehicle locally, what would I actually have to shop against?”

Present the counter offer like a professional

Your counter package should be organized and short enough to read. Don't send a rambling email with ten disconnected complaints.

A useful structure looks like this:

- State the dispute clearly. Identify the claim, vehicle, and the insurer's offer.

- List the report errors. Incorrect comps, wrong condition, missing options, non-local listings, unsupported deductions.

- Attach your evidence. Photos, receipts, service records, and local comparables.

- State the revised value. Tie it to your evidence, not emotion.

- Request correction or appraisal. If the insurer won't adjust voluntarily, move the file forward.

A clean, evidence-based package changes the conversation. It tells the insurer you're not guessing, and it creates a record that matters if the dispute proceeds to appraisal.

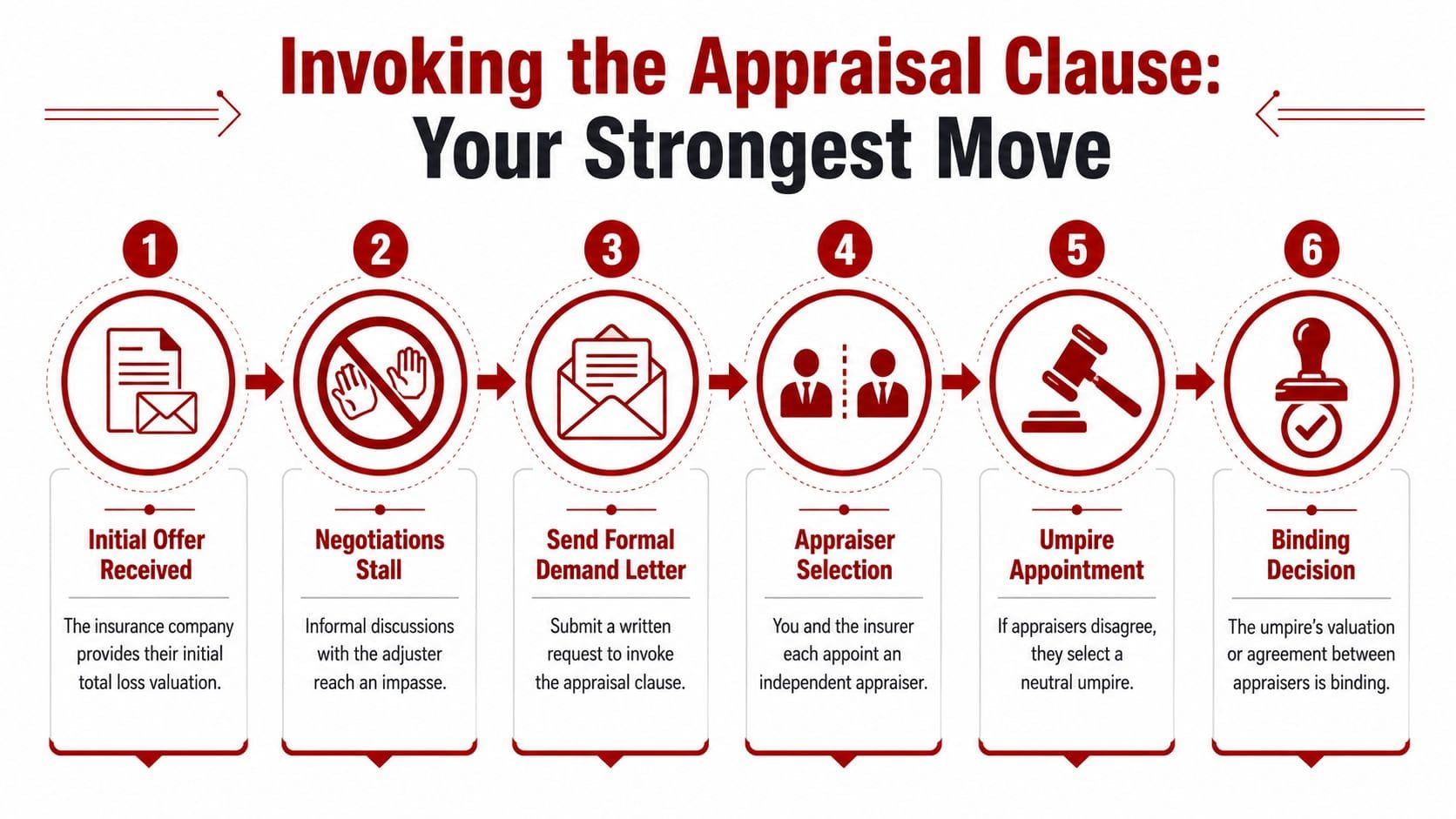

Invoking the Appraisal Clause Your Strongest Move

When the adjuster keeps repeating the same low valuation, it's time to stop negotiating in circles. The appraisal clause is usually the strongest contractual tool you have in a pure value dispute.

Why the appraisal clause changes the leverage

Informal negotiation keeps the insurer in control of the pace and framing. The appraisal clause changes that. It moves the dispute out of casual adjuster discussion and into a structured valuation process between appraisers.

That matters because valuation disputes should be decided by valuation evidence.

In Oregon, the appraisal route is often productive. Invoking the appraisal clause has a high success rate, with policyholders seeing an average settlement increase of 18–25% over the insurer's initial offer by using a certified appraisal to correct flawed comparable selections, according to Oregon total loss appraisal data.

The clause isn't hostile. It's procedural. You're not accusing anyone of misconduct by invoking it. You're saying the parties disagree on value and the policy provides a mechanism to resolve that disagreement.

What to send the insurer

The letter or email should be direct and calm. Short is better.

Include these points:

- Identify the claim and vehicle. Claim number, year, make, model, VIN.

- State the disagreement. Say you dispute the insurer's total loss valuation.

- Invoke the appraisal clause expressly. Use those words.

- Ask for confirmation in writing. Request the insurer's appraiser information and next procedural steps.

- Reserve your rights. Don't sign releases while value remains disputed.

A basic form of wording works:

I dispute your valuation of my vehicle's actual cash value and formally invoke the appraisal clause under my policy. Please confirm receipt, identify the appraiser selected on behalf of the insurer, and provide any additional procedural requirements you contend apply.

This step also helps owners in Washington when the policy includes appraisal language, though the exact wording and process should always be checked against the policy itself.

If you don't want to manage the appraisal demand, evidence package, and appraiser-to-appraiser negotiation yourself, some owners use firms that handle the entire process, including total loss appraisal services, from valuation review through negotiation and, if necessary, umpire coordination.

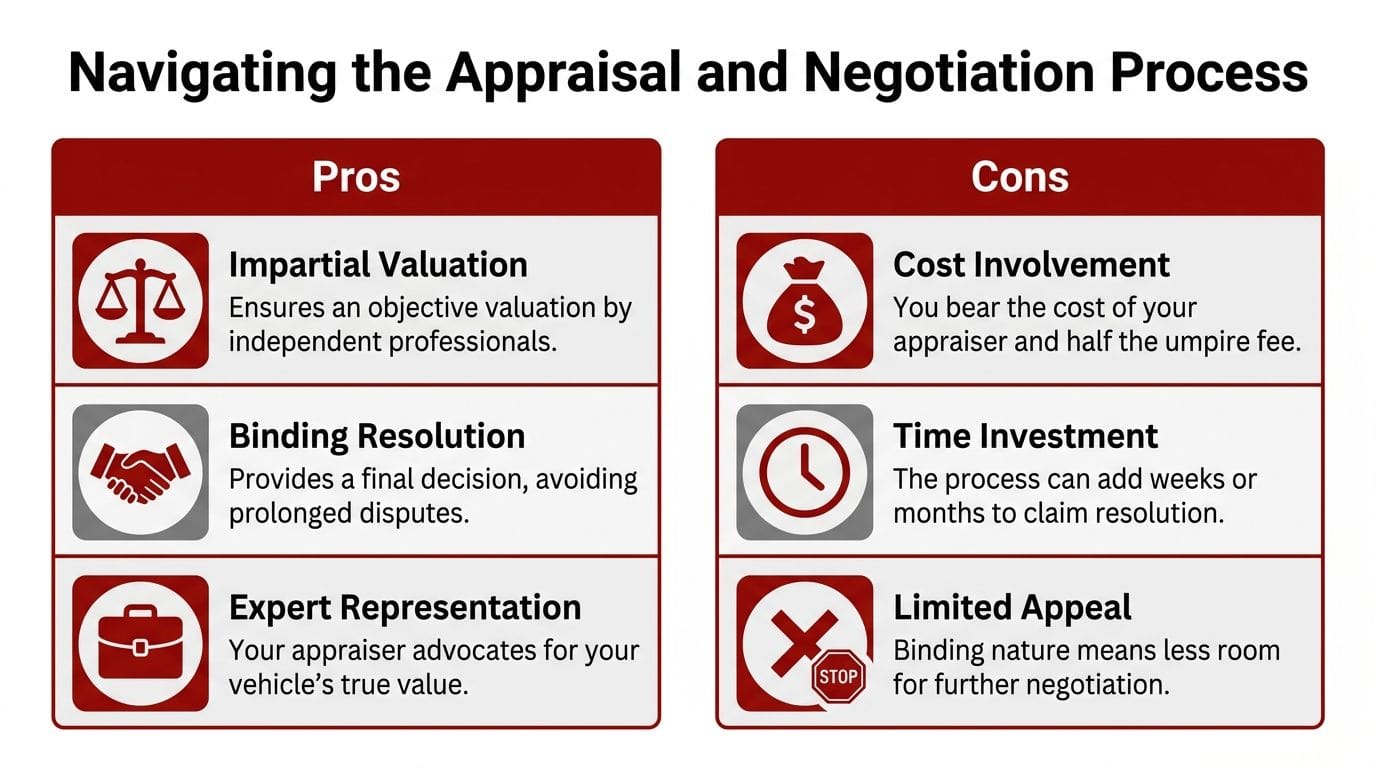

Navigating the Appraisal and Negotiation Process

Once appraisal starts, the dispute becomes more technical and less theatrical. That's good for owners with real evidence.

Choose your appraiser carefully

Not every appraiser approaches a total loss dispute the same way. Some do basic form reports. Some work both sides of the aisle. Some understand niche vehicle markets. Some don't.

The practical difference is independence and depth.

Ask these questions before hiring anyone:

| Question | Why it matters |

|---|---|

| Do you work for insurers or valuation vendors? | You want to understand possible conflicts |

| Do you review CCC ONE or Mitchell reports line by line? | Many disputes turn on report-specific errors |

| Do you research local replacement vehicles? | Local market analysis is often the core issue |

| Do you negotiate directly with the insurer's appraiser? | Process management matters as much as the report |

Your appraiser's job is not just to write a higher number. It's to support a defensible market value and negotiate from evidence that can survive scrutiny.

How the negotiation usually unfolds

After both sides name appraisers, the exchange begins. Reports, comparable vehicles, condition analysis, option corrections, and local market support all come into play. At this point, a weak insurer file often starts to show strain.

Most of the useful work happens off the phone and off the claim portal. It happens in the quality of the comparables, the corrections to the valuation inputs, and the persistence of the negotiation.

There's also an important Oregon protection that changes the risk calculation for owners. Under Oregon law, insurers must reimburse your reasonable appraisal costs if the final settlement value is even $1 higher than their last offer, as explained in this review of Oregon total loss appraisal cost reimbursement. That's a powerful rule because it removes much of the financial downside of challenging a low offer.

Don't evaluate appraisal only by the fee. Evaluate it by the difference between accepting a suppressed valuation and forcing a market-supported one.

The process can still take time. It may add weeks. It may require follow-up and patience. But compared with endless informal arguing, it usually puts the dispute on firmer ground.

If you want another consumer-oriented perspective on tactics before or during negotiations, this guide on how to negotiate insurance settlement effectively is a useful supplemental read.

Escalation Strategies Umpire and Legal Options

Most appraisal disputes settle before the final escalation step. But you should know what happens if the two appraisers don't agree.

When an umpire gets involved

An umpire is the neutral third party used to break a deadlock. If your appraiser and the insurer's appraiser can't reconcile the value dispute, they submit the disagreement to the umpire under the appraisal process set by the policy.

The umpire doesn't redo everything from scratch in the abstract. The umpire reviews the competing evidence and decides the disputed valuation issues. That may mean siding mostly with one appraiser, blending positions, or resolving a narrow set of disputed adjustments.

For owners, the practical point is this: a disagreement between appraisers does not mean the process failed. It means the process has another decision-maker built in.

When to challenge the total loss decision itself

Sometimes the right move isn't only to challenge the total loss offer. It's to challenge the total loss declaration.

That issue comes up when the repair estimate looks bloated, the salvage figure looks suspicious, or the vehicle is late-model, specialty, or otherwise worth preserving. A vehicle owner who wants repair instead of a total can ask for the worksheet and supporting numbers behind the total loss decision.

A little-known tactic is to demand the adjuster's worksheet to test whether the repair estimate was inflated to trigger the state's total loss threshold, as discussed in this article on challenging total loss settlement strategy and adjuster worksheets.

That request can matter a lot in disputes involving:

- Specialty trucks or diesels: Small spec errors can distort value and total-loss math.

- Older but desirable vehicles: Retail demand may exceed what generic valuation tools recognize.

- Repairable vehicles with disputed estimates: Body labor, parts sourcing, and procedure assumptions can affect the threshold calculation.

When a lawyer makes sense

An attorney is not necessary for every valuation dispute. In many cases, appraisal handles the problem more efficiently than litigation.

Legal counsel becomes more relevant when the dispute goes beyond value. Examples include a coverage denial, a refusal to honor the appraisal clause, a release problem, title issues, or conduct that looks like bad faith rather than a routine valuation disagreement.

If you're unsure whether you need an appraiser, an umpire, or a lawyer, start with the narrowest question first: is this a disagreement about value, or is it a disagreement about coverage and claim handling? That distinction saves time and money.

If you need help building the evidence, dissecting a CCC ONE or Mitchell report, or moving a stalled claim into appraisal, Leverage Auto Appraisals handles Oregon and Washington total loss disputes for vehicle owners, including valuation review, appraisal clause invocation, negotiation with the insurer's appraiser, and umpire escalation when required.