Airbag deployment does not automatically total a car. What decides it is the money: if repair costs, including airbag replacement, push the claim up to your vehicle's actual cash value, the insurer may treat it as a total loss, and a single airbag alone often costs $750 or more to replace.

If you're reading this right after a crash, you're probably staring at a damaged car, a warning light, and an insurance process that suddenly feels stacked against you. The moment airbags deploy, most owners assume the decision has already been made. It hasn't.

In Oregon and Washington, that assumption can cost you money because the main fight usually isn't over whether the airbags went off. It's over what your vehicle was worth before the crash, how the repair estimate was built, and whether the insurer's valuation leaves money on the table. Those are very different questions, and they give you more room to act than most adjusters explain up front.

Table of Contents

- The Real Answer to the Airbag Question

- How Insurers Actually Calculate a Total Loss

- The True Cost of Airbag System Replacement

- Oregon and Washington Total Loss Rules

- Your Action Plan After Receiving an Offer

- Protecting Your Investment and Ensuring a Fair Payout

The Real Answer to the Airbag Question

The short answer to “does airbag deployment total a car” is no. Airbags deploying is a serious cost signal, not an automatic legal trigger.

That distinction matters because many owners give up too early. They hear “airbags went off” and assume the car is done, the insurer's number is final, and the only choice is to sign the paperwork. In practice, the insurer still has to run a financial calculation.

Airbag deployment increases the chance of a total loss because those parts cannot be reset and reused. Replacement costs stack up fast. If one bag costs around $750, multiple deployed airbags can create thousands of dollars in repair expense before body work, interior repair, diagnostics, or recalibration are even fully accounted for, as noted by Toyota of Clermont's explanation of deployed airbags and total loss decisions.

What owners usually get wrong

The most common mistake is focusing only on the crash severity. That's understandable, but insurers don't total a vehicle because the accident looked violent. They total it when the economics stop making sense under the applicable rules.

A newer, higher-value vehicle can absorb a large repair bill and still be repairable. An older vehicle with a lower market value can tip into total-loss territory with much less visible damage because the airbag system adds so much expense.

Practical rule: Don't ask only, “Did the airbags deploy?” Ask, “What is the full repair estimate, and what is the insurer saying my car was worth one minute before the crash?”

That second number is where owners in Oregon and Washington often have an advantage. If the insurer undervalues your car, the whole decision tree shifts in the carrier's favor. A lower value makes it easier for them to declare a total loss and easier to justify a smaller payout.

What actually determines the outcome

The outcome usually turns on three things working together:

- Repair scope: Airbags, seatbelt components, dash or steering wheel damage, sensors, wiring, and body damage all affect the estimate.

- Pre-loss value: The insurer's view of your vehicle's actual cash value drives the claim.

- State rule: Oregon and Washington use their own standards, which can differ from percentage-based rules people read about elsewhere.

If you own the car outright, a low valuation directly affects your pocket. If you still have a loan, it can affect whether your payoff leaves you short.

A deployed airbag is often the event that starts the total-loss conversation. It is rarely the only reason the claim lands there.

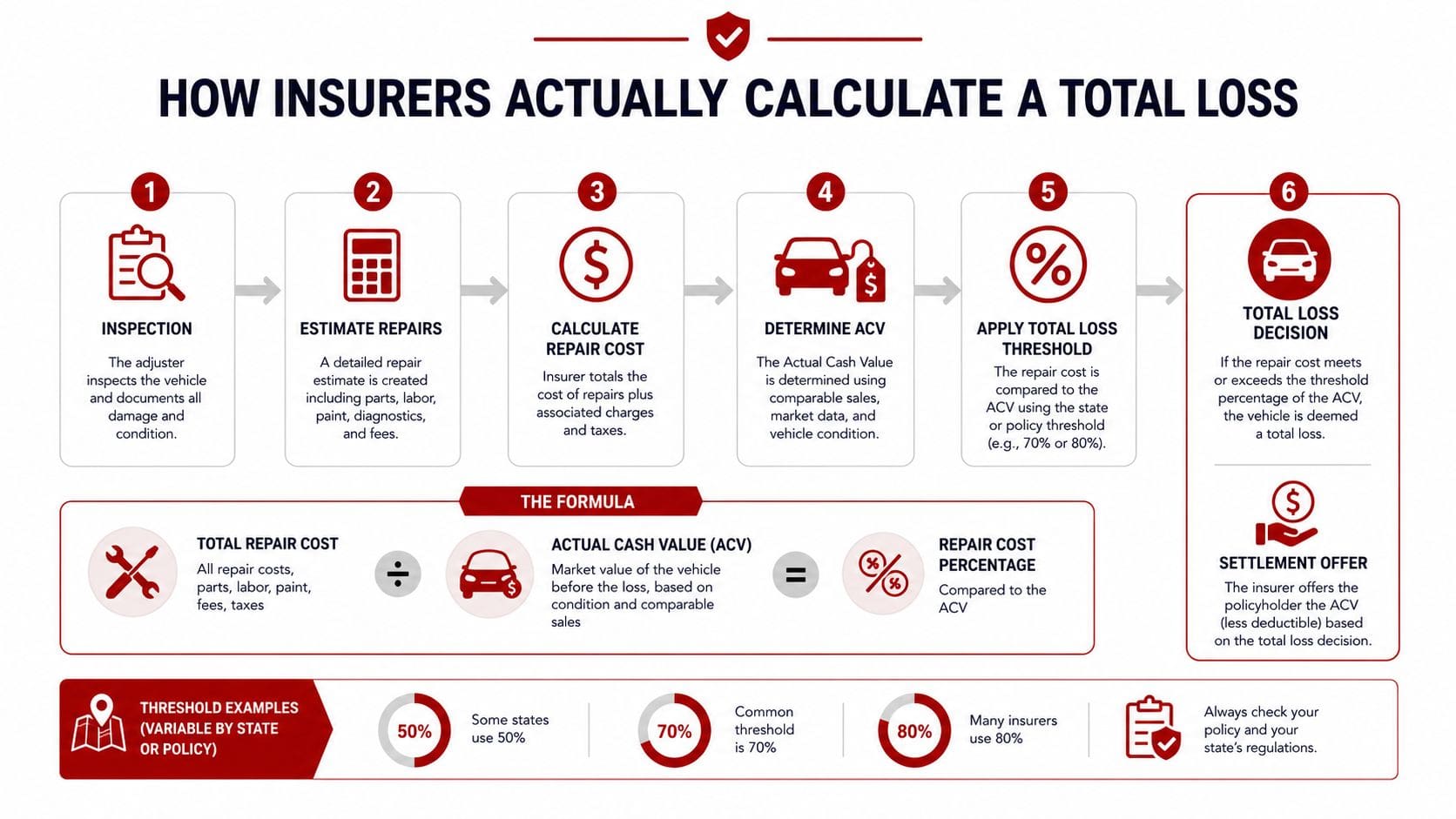

How Insurers Actually Calculate a Total Loss

Insurance companies don't start with the airbag. They start with a comparison between the cost to repair and the vehicle's actual cash value, or ACV.

The formula behind the decision

Consider a major home repair. If repairing a damaged roof and structure costs as much as the house is worth, the insurer won't keep pouring money into repairs. Vehicle claims work the same way.

Airbag deployment alone doesn't automatically total a car. The key question is whether total repair costs, including airbag replacement, sensor recalibration, and structural repair, equal or exceed the vehicle's ACV under state total-loss rules. In Oregon, ORS 819.012 uses that equal-or-exceed standard, and Washington applies the same fair-market-value rule under RCW 46.12.600, as summarized in Toyota of North Charlotte's discussion of total-loss calculations.

That sounds clean on paper. It rarely feels clean to the owner because both sides of that equation can move. The repair estimate can grow once hidden damage is found. The ACV can shrink if the insurer uses weak comparable vehicles, misses options, or grades the condition too harshly.

Why ACV becomes the pressure point

Most clients focus first on the body shop number. I understand why. It's concrete. But the repair side is often less negotiable than the value side.

Actual cash value is not what you paid for the car. It's not what you still owe. It's not what you hoped to sell it for. It is the insurer's estimate of what your vehicle was worth immediately before the accident based on factors like year, make, model, mileage, equipment, prior condition, and local market evidence.

That's why it helps to understand the difference between valuation methods before a claim ever happens. If you want a plain-language comparison, this guide to choosing the right policy gives a useful overview of ACV versus agreed value coverage.

When the insurer undervalues ACV, three things happen at once:

- The vehicle reaches total-loss territory faster

- The payout drops

- Your negotiating position weakens unless you challenge the report

Don't treat the valuation report like boilerplate. Read it like an invoice someone expects you to approve with your money.

Look for missing options, wrong trim level, inaccurate mileage, condition deductions that don't match the vehicle, and comparable sales from markets that don't reflect where your car would realistically be bought and sold.

The True Cost of Airbag System Replacement

A deployed airbag rarely means one part and one bill. In Oregon and Washington claims, I often see owners focus on the torn steering-wheel bag or the split dashboard, while the estimate that decides the claim is built from the whole safety system.

Once the airbags go off, the shop may need to replace the steering wheel airbag, passenger dash module, seatbelt pretensioners, impact sensors, control module, trim pieces, and sections of the dash or seats. Then the system has to be scanned, repaired correctly, and verified so the restraint system will work again in a second crash. On newer vehicles, calibration work can add more cost after the visible repairs are done.

That is why airbag claims turn older vehicles into financial edge cases so quickly. The bag itself is only part of the number. Labor, diagnostics, related safety components, and interior replacement parts are what push the estimate up.

Why the estimate grows faster than owners expect

Here is a common example. A front-end crash triggers the driver airbag and passenger airbag. The seatbelts lock up. The passenger bag breaks through the dash pad. The control module stores the crash event and may need replacement or reset, depending on the vehicle and repair method the carrier accepts. The front bumper, grille, headlamp, hood, and reinforcement bar also need repair.

At that point, the question is not whether the airbag deployed. The question is whether the full repair total still makes financial sense against the vehicle's pre-loss value.

That distinction matters in Oregon and Washington because owners often have room to challenge the value side of the equation if the insurer is leaning toward a total loss. If you are sorting through that process, this guide to an Oregon total loss appraisal and valuation dispute can help you see where the pressure points usually are.

Sample airbag system replacement costs

Below is a simple cost framework using only the figures supported earlier in the article.

| Component | Average Cost per Unit | Notes |

|---|---|---|

| Single airbag | Around $750 | Airbags cannot be reused and must be replaced |

| Four airbags | $3,000 | This is the bag replacement cost alone before other repairs |

| Full airbag system replacement | Can exceed $10,000 | May include inflators, sensors, wiring, and related system work, especially in newer vehicles |

The practical issue for owners is straightforward. A ten-year-old car with modest market value can cross into total-loss territory from safety-system work before the body estimate looks severe. A late-model SUV with strong market value may support the same repair bill without being totaled.

Where owners in Oregon and Washington can protect themselves

I advise clients to slow down and read the paperwork, not the headline number.

Ask for the full line-item estimate. Confirm whether the insurer included OEM or aftermarket parts where allowed, whether seatbelt components are on the sheet, whether dash replacement is included, and whether scans and calibrations were priced. Then compare that repair total to the insurer's valuation report, because that is where your legal and financial advantage usually sits in Oregon and Washington.

A few practical points matter here:

- Older vehicles face a harder math problem. Airbag and seatbelt repairs can consume a large share of the vehicle's value quickly.

- Multiple deployment points raise costs fast. Side curtains, seat airbags, and pretensioners can turn a moderate collision into a major safety-system repair.

- Higher-value vehicles give you more room. The same restraint-system bill that totals an older sedan may still be repairable on a newer truck or SUV.

- The estimate is not the only number to verify. If the insurer undervalued your car, a total-loss decision can be based on weak valuation work, not just expensive repairs.

If you want to know whether the airbags drove the total-loss decision, ask for the estimate and the valuation report together. Reviewing only one of those documents leaves out half the story.

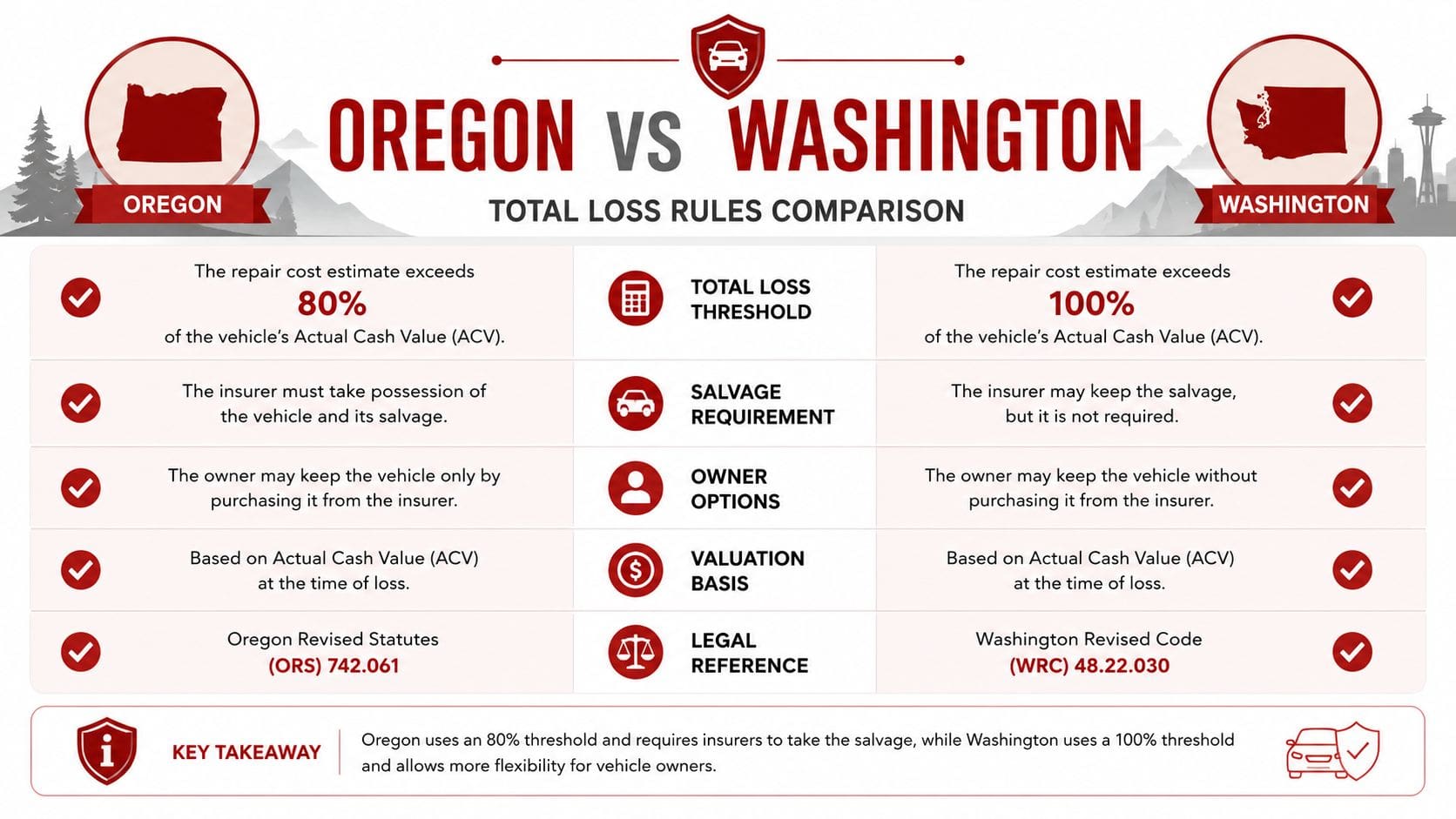

Oregon and Washington Total Loss Rules

For Oregon and Washington owners, local law matters more than generic advice from national forums. A lot of online content talks about percentage thresholds without explaining that your state may handle total loss decisions differently.

Whether a car is totaled depends on repair costs versus pre-accident ACV. In Oregon (ORS 819.012) and Washington (RCW 46.12.600), a car is totaled if repair costs equal or exceed ACV. Many other states use a Total Loss Threshold, often 70% to 80% of ACV, and airbag replacement costing over $750 per bag can push older vehicles over those thresholds, as summarized in D'Amore Law Group's overview of airbags and total-loss determinations.

Why local law matters more than internet advice

If someone in another state says, “My car was totaled at seventy-five percent,” that may be true for their claim and irrelevant to yours. Oregon and Washington owners need to think in terms of value equality, not just a lower percentage trigger.

That creates a practical advantage. If the insurer is saying your Oregon or Washington vehicle is a total loss, the value number becomes especially important because even a modest increase in ACV can materially affect the claim outcome or at least the payout amount.

For Oregon readers who want a closer look at how this works in practice, this Oregon total loss guide breaks down the local framework in more detail.

What owners can do with that knowledge

Use the law to sharpen your questions. Don't ask the adjuster broad questions like “Why is this totaled?” Ask targeted ones:

- What ACV are you using?

- What comparables support that number?

- What exact repair total are you relying on?

- Did you account for all factory options and condition correctly?

Many owners secure an advantageous position. The insurer may be right that the vehicle qualifies as a total loss under Oregon or Washington rules. But they still have to pay a fair ACV. Those are separate issues, and you shouldn't let the first one distract you from the second.

Your Action Plan After Receiving an Offer

Once the insurer sends the valuation or total-loss offer, slow down. Most bad outcomes start when owners assume the first number is objective, complete, and not worth challenging.

What to do before you accept anything

Start with the paperwork, not the phone call. Ask for the full valuation report and the repair estimate in writing. Many carriers rely on systems such as CCC ONE or Mitchell-style valuation reports. You need the underlying details, not just the settlement number.

Then review the report like a buyer would review a used-car listing.

Verify the basics

Check year, make, model, trim, drivetrain, mileage, and VIN-related equipment. One wrong trim level can pull the valuation down fast.Check factory and added equipment

Leather, premium wheels, towing equipment, driver-assist packages, diesel packages, upgraded audio, bed accessories, and similar items are often missed or undervalued.Read the condition adjustments closely

If the report applies deductions for condition, ask what evidence supports them. A generic downgrade shouldn't stand if your vehicle was well kept.

The first offer is often a starting position, not a final answer.

How to challenge the valuation effectively

A strong dispute is organized. Emotion is understandable, but documentation wins.

Build your response with evidence the insurer can't dismiss easily:

- Comparable vehicles: Find like-kind local listings with similar trim, mileage, and equipment.

- Service records: Maintenance records help show condition and support the idea that your car wasn't average or neglected.

- Photos before the crash: Clear pre-loss photos can undercut exaggerated condition deductions.

- Receipts for recent work: Tires, mechanical work, and certain upgrades may support condition and marketability, even if they don't translate dollar-for-dollar.

Write a concise rebuttal. Point out each error specifically. Don't send a long rant. Send a clean list of corrections and attach the supporting documents.

If you're trying to understand the dispute process from the owner's side, this guide on how to challenge a total loss offer is a useful reference point.

When the appraisal clause matters

If the insurer won't correct the valuation after you present evidence, check your policy for the appraisal clause. This is a contractual process that can allow each side to hire its own appraiser to determine value.

That matters because most owners hit the same wall at the same point. The adjuster repeats the original valuation, says the report is vendor-supported, and frames the number as settled. It isn't necessarily settled if your policy gives you appraisal rights.

What works here is being deliberate:

- Read the policy language: Confirm whether your policy includes an appraisal clause and how it must be invoked.

- Keep communications in writing: Email creates a clean record.

- Separate value from liability issues: The appraisal clause usually concerns value disputes, not fault disputes.

- Move before storage and rental pressure forces a rushed decision: Insurers know time pressure changes behavior.

If the insurer won't negotiate on evidence, your leverage often comes from process rights, not repeated phone calls.

A disciplined owner can improve a claim outcome by catching report errors early. A well-run appraisal process can go further because it moves the dispute into a formal value-setting mechanism rather than an open-ended adjuster conversation.

Protecting Your Investment and Ensuring a Fair Payout

A total-loss letter often arrives when you are still dealing with towing, rental deadlines, and questions about whether the car can be repaired. That is exactly when owners in Oregon and Washington make expensive mistakes. The insurer's first number may be workable, but it may also be low because the options list is wrong, the condition rating is too harsh, or the comparable vehicles are weaker than your vehicle.

Your financial interest usually turns on actual cash value, not the airbag deployment by itself. If the carrier totals the vehicle, the next question is whether the settlement reflects the pre-loss value of your car, truck, or SUV. That is where documentation matters. Window sticker details, service records, recent major repairs, photos, trim level, factory packages, tire condition, and local comparable sales can all affect the payout.

If you need a practical starting point, this guide to how to dispute total loss value in Oregon explains the process in plain terms.

I tell clients to treat the valuation report like an estimate that needs to be checked, not a final answer that has to be accepted. A polished report can still contain the wrong drivetrain, missed safety or technology packages, prior-condition assumptions that are too low, or comparable vehicles from outside the proper market area. In Oregon and Washington, those details can move the settlement enough to justify a careful review, especially on newer vehicles, specialty trims, and well-kept older cars.

Do not sign a release until you understand what you are giving up.

If you want an independent review before accepting a total-loss settlement, our firm, Leverage Auto Appraisals, helps Oregon and Washington vehicle owners evaluate insurer valuations, challenge low offers, and handle appraisal clause disputes with market-based support.