Your car is gone, the tow yard is calling, and the insurer just emailed a number that won't buy anything close to what you had. That's where individuals often find themselves in a total loss settlement dispute. They're tired, under time pressure, and talking to an adjuster who acts like the valuation report is objective and final.

It isn't final.

In Oregon and Washington, the significant advantage often begins after the first offer. The policy is a contract. If the value is wrong, you can challenge it. If the adjuster stops moving, the appraisal clause can take the dispute out of the usual back-and-forth and put it into a process where evidence matters more than persistence.

Table of Contents

- Your Rights After a Lowball Total Loss Offer

- How to Build Your Evidence Package

- Invoking the Appraisal Clause to Force a Resolution

- Why an Independent Appraiser is Your Best Weapon

- Navigating the Final Appraisal and Umpire Process

- Taking Control of Your Total Loss Settlement

Your Rights After a Lowball Total Loss Offer

A low offer feels personal, but it usually comes from a process problem. The insurer often relies on a valuation system such as CCC ONE or Mitchell, then an adjuster reviews the report and presents the number as Actual Cash Value, or ACV. That number may look polished. It may still be wrong.

The first thing to understand is that ACV is supposed to reflect what your vehicle was worth in your market before the loss, not what an algorithm can defend with weak comparisons. If the report uses the wrong trim, misses options, overstates prior condition issues, or pulls vehicles from the wrong area, the number drops fast.

What Oregon policyholders need to know first

Oregon gives you a very clear benchmark on when a vehicle qualifies as a total loss. A vehicle is legally declared a total loss when the cost to repair it reaches or exceeds 80% of its ACV, using the formula Repair Cost + Salvage Value > ACV, under the state standard explained in this Oregon total loss threshold guide.

That matters for two reasons.

First, it tells you the insurer doesn't get to wave a hand and total the car without a framework. Second, it reminds you that valuation sits at the center of the claim. If ACV is too low, the entire total loss decision and settlement amount can skew against you.

Practical rule: Never argue only that the offer feels unfair. Argue that the report is unsupported, incomplete, or out of line with the local market.

What Washington drivers should focus on

Washington policyholders deal with the same practical problem even if the legal framework isn't identical to Oregon's threshold rule. The key issue is still valuation quality. You need to know whether the insurer used real local retail vehicles, whether the options match, and whether the mileage and condition adjustments make sense.

That shifts your role from frustrated owner to document reviewer.

Use this quick checklist before you respond to the adjuster:

- Request the full valuation report: Don't settle from a summary screen or phone call.

- Confirm the vehicle identity: Year, make, model, trim, drivetrain, packages, and mileage all need to be right.

- Check every comparable: Location, seller type, options, and asking context matter.

- Review deductions carefully: Condition adjustments often get accepted without proof.

- Read your policy: Look for the appraisal clause and any instructions for invoking it.

The first offer is a starting line

A lot of people lose ground because they treat the insurer's first number as a final decision instead of an opening position. In a total loss settlement dispute, that's a mistake. The insurer has a process. You need one too.

Start by slowing the claim down just enough to review the paperwork. Don't cash anything labeled as full settlement until you understand what rights you may be giving up. Don't rely on the adjuster to explain your options cleanly. And don't assume more phone calls will fix a valuation report built on bad inputs.

A strong dispute starts with a simple mindset: the report is evidence, not truth.

How to Build Your Evidence Package

Good negotiation in a total loss settlement dispute doesn't start with a speech. It starts with a file. If your documents are thin, the insurer can brush you off. If your file is organized and local, the adjuster has to respond to substance.

The most common valuation flaw is the use of non-local or wholesale data, and a proper audit of comparable vehicles means checking location, options, and mileage adjustments. When policyholders counter with local retail evidence, the result typically yields 12–18% increases over initial offers, according to this analysis of total vehicle claim valuation methods.

Start with records that prove what your car was

Think like you're documenting the vehicle for someone who has never seen it.

Gather these first:

- Ownership records: Title, registration, payoff information if there's a lender, and purchase paperwork.

- Condition proof: Pre-loss photos, detail photos, service records, and inspection reports if you have them.

- Recent money spent: Tires, brakes, suspension work, timing components, battery replacement, and major repairs.

- Factory and aftermarket equipment: Tow packages, premium trim features, diesel upgrades, camper shells, wheel packages, or specialty accessories that affect market appeal.

If you're missing old sales documents, a practical resource like this guide to car transaction paperwork can help you identify what records may still be worth tracking down.

Audit the insurer's comparables like a skeptic

It is common to glance at the comp list and stop at the prices. That's not enough. You need to ask whether each comp belongs in the report at all.

Look at the insurer's list and mark up every issue you find:

| Checkpoint | What to look for | Why it matters |

|---|---|---|

| Location | Same local market, not distant listings | Remote comps can depress value |

| Seller type | Retail dealer listings vs wholesale context | ACV disputes should center on replacement market evidence |

| Vehicle match | Trim, cab configuration, drivetrain, engine, packages | Small mismatches create big value differences |

| Mileage | Reasonable comparison to your actual odometer | Bad mileage adjustments drag value down |

| Condition | Real support for any downward deduction | Unsupported condition hits are common |

If a comparable wouldn't have made your own shopping list before the loss, question why it's in the report now.

Build your own local comp set

Your replacement comps should be clean, current, and as close to like-for-like as you can get. Save screenshots or PDFs. Capture the VIN when available. Keep the dealer name, city, listed mileage, and visible options.

A workable package usually includes:

- Local retail listings that reflect what a buyer in your area would face.

- A short note on each comp explaining why it matches your vehicle.

- A rebuttal sheet pointing out each error in the insurer's report.

- Supporting records for condition and maintenance.

For Oregon owners dealing with this process, this overview of how to dispute total loss value in Oregon is a useful reference point for organizing the challenge.

What doesn't work well

Some evidence feels persuasive but usually doesn't move the claim much on its own.

- Book values alone: Kelley Blue Book or Edmunds can help you orient yourself, but they don't replace local market proof.

- General complaints about used car prices: Adjusters hear that every day.

- A pile of unsorted screenshots: If the evidence is messy, it loses force.

- Emotion without documentation: Your attachment to the vehicle is real. The valuation process still turns on market evidence.

The strongest package is boring in the best way. It's specific, local, and hard to dismiss.

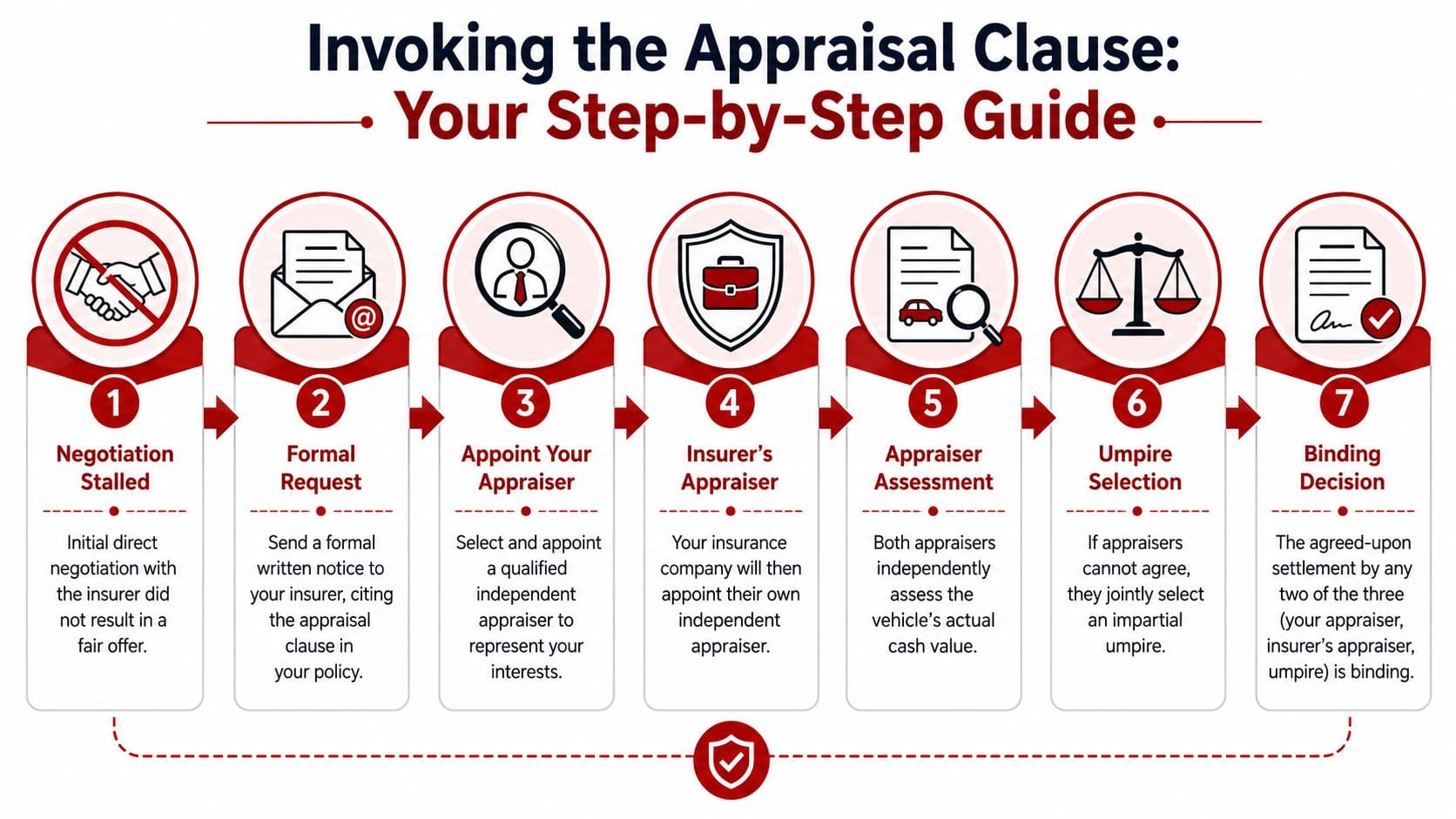

Invoking the Appraisal Clause to Force a Resolution

There's a point where more negotiation stops being productive. You've sent records. You've pointed out bad comps. The adjuster either repeats the same number or makes a token movement and hopes you'll give up. That's when the appraisal clause becomes more than policy language. It offers significant bargaining power.

Most guides mention the clause and move on. That misses the whole point. The appraisal clause is a contractual right that forces a binding resolution on value disputes, and it has become the main defense consumers have against automated valuation tools and insurer refusal to negotiate, as explained in this guide on undervalued total loss claims and appraisal strategy.

When it makes sense to invoke it

You don't need to wait forever. In practice, the right time is usually when the dispute is clearly about value and the insurer has had a fair chance to correct obvious issues.

Common signs it's time:

- The adjuster won't explain the calculation

- The report contains mismatched or distant comparables

- Your documentation gets ignored rather than addressed

- The insurer insists the software result is the market

- Conversations keep repeating without any meaningful change

At that stage, continuing to argue with the same adjuster can waste time. A formal appraisal demand changes the audience and the process.

How to invoke the clause in writing

Keep it direct. Don't write a manifesto. Write a clear notice.

A simple version looks like this:

I dispute your valuation of my vehicle's Actual Cash Value and formally invoke the appraisal clause under my policy. Please confirm receipt, identify any policy-specific requirements you contend apply, and provide the name and contact information for the appraiser your company designates.

That kind of notice does three things. It creates a paper trail. It signals that you understand this is a contractual process. And it stops the claim from staying trapped in endless informal negotiation.

If you want a local reference on the Oregon side of these disputes, this Oregon total loss appraisal information page lays out the issue in practical terms.

Why this works better than asking again

Adjusters manage volume. Appraisal changes the incentive structure. Once invoked properly, the insurer usually has to engage in a defined process rather than just defend the first report.

That matters because value disputes improve when the discussion moves away from call-center scripts and toward evidence review.

A few things to keep in mind:

- Appraisal is about value, not fault: It won't fix a liability dispute.

- Writing matters: Oral statements can vanish. Email and letters don't.

- Timing matters too: Don't sit on your rights while storage, rental issues, or financing pressure build.

- Professional help can matter early: A clean invocation paired with a strong package often avoids a harder fight later.

The big shift is psychological as much as procedural. You stop asking the adjuster to reconsider. You start enforcing the contract.

Why an Independent Appraiser is Your Best Weapon

Once the appraisal clause is in play, the dispute stops being a casual argument about what your car was worth. It becomes a technical valuation contest. That's where most owners are outmatched if they go in alone.

An independent appraiser's job isn't to make noise. It's to build a valuation that holds up when the insurer's appraiser pushes back on every line item.

The difference is structure. A professionally prepared package should include a licensed appraiser's report, local retail comps, and a line-by-line rebuttal of the insurer's valuation. When policyholders use that approach, success rates for resolving total loss disputes exceed 85%, and umpire escalation is needed in fewer than 5% of cases, according to this independent appraisal dispute guidance.

What a good appraiser actually does

A qualified appraiser doesn't just “give you a number.” The work usually includes:

- Verifying vehicle identity: Trim, drivetrain, factory equipment, and prior condition.

- Researching local replacement market evidence: Not generic national averages.

- Reviewing the insurer's CCC ONE or Mitchell report: Especially comp selection and adjustments.

- Writing a defensible report: Clear enough to negotiate from, detailed enough to survive challenge.

- Speaking appraiser to appraiser: That is often underestimated.

In Oregon and Washington, local knowledge helps. Market behavior for a diesel truck, an all-wheel-drive SUV, or a clean late-model commuter car isn't identical from region to region. A local appraiser should understand those demand differences and know how to document them.

One available option for owners who want representation in that process is an independent total loss appraiser service, which handles valuation review and negotiation under the appraisal clause.

What to look for before you hire anyone

Not every appraiser is a good fit for a total loss settlement dispute. Ask practical questions.

| Question | Why it matters |

|---|---|

| Do you work only for vehicle owners? | Conflicts matter in valuation disputes |

| Do you handle total loss claims regularly? | Total loss work is different from general appraisals |

| Will you rebut the insurer's report line by line? | General opinions aren't enough |

| Do you negotiate directly with the insurer's appraiser? | The report alone may not close the gap |

| Are you familiar with Oregon and Washington claim practice? | Local process knowledge saves time |

Worth remembering: You are not hiring someone to “complain better.” You're hiring someone to document value in a way the other side has to answer.

A quick video can help make that role more concrete:

Why owners struggle without one

For an individual, this is often a singular event. The insurer's side sees these reports every day. They know how the valuation software is defended, how adjustments get framed, and which owner objections are easy to brush aside.

Without an appraiser, owners often make the same mistakes:

- They focus on what they owe instead of market value.

- They use broad pricing sites instead of local retail comparables.

- They miss small report errors that stack into a lower ACV.

- They escalate emotionally, then lose credibility with the person reviewing the file.

A solid independent appraisal changes the dynamic because it moves the dispute out of opinion and into evidence.

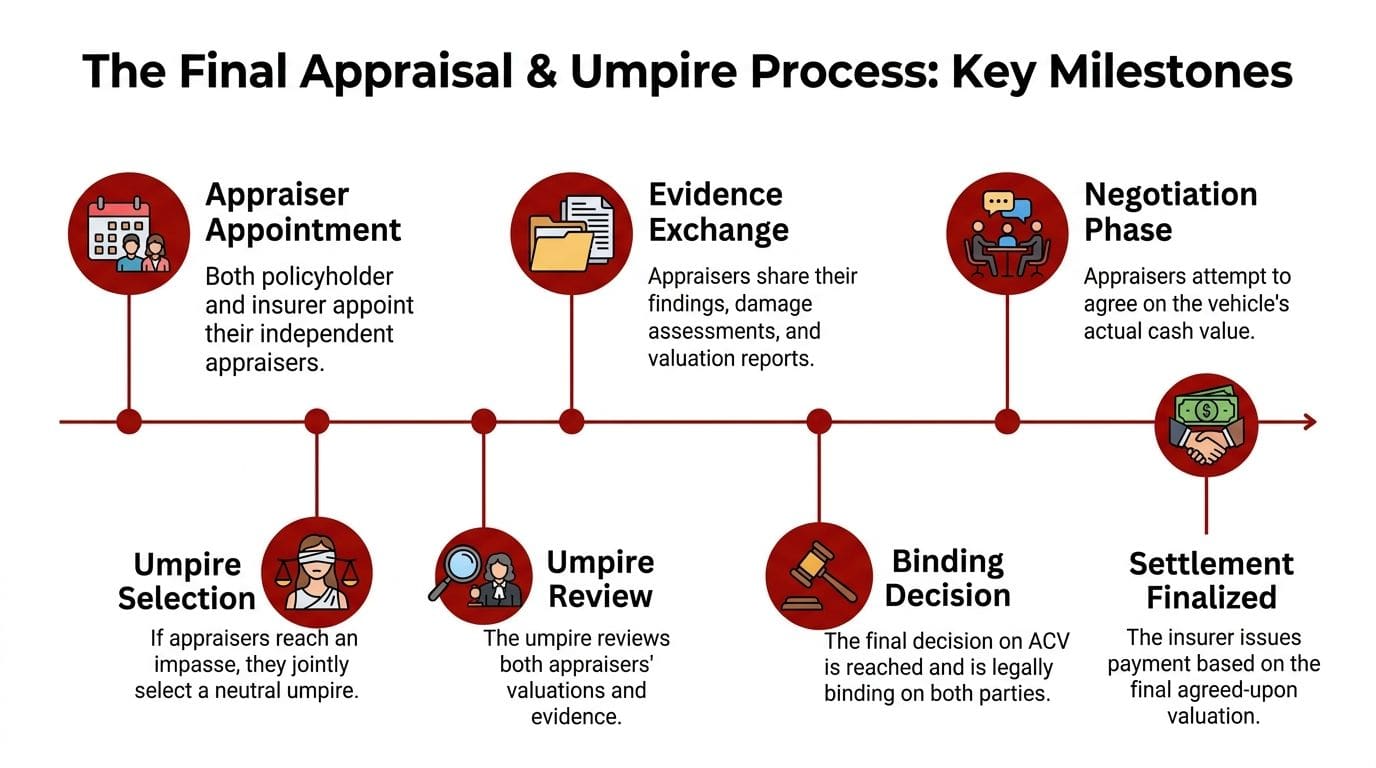

Navigating the Final Appraisal and Umpire Process

Once both sides appoint appraisers, the claim enters a more formal lane. That sounds intimidating until you see how it usually unfolds. It's not a courtroom. It's a structured valuation process, and in many cases the two appraisers resolve it without ever needing an umpire.

It often starts subtly. Your appraiser reviews the insurer's file, builds a competing valuation, and sends over the support. The insurer's appraiser studies it, compares notes against their own report, and the substantive negotiation begins. This stage is where weak comps, unjustified deductions, and missed equipment usually get tested hard.

What the back and forth often looks like

The first exchange is rarely dramatic. One side says a comp is too far away. The other says it's still relevant. One side says the mileage adjustment is excessive. The other asks for support. Then the file gets tighter.

That process usually centers on a handful of practical questions:

- Was the vehicle matched correctly?

- Are the comparables local and retail?

- Did the insurer understate condition or equipment?

- Do the adjustments make sense in the market?

Most appraisal disputes are won in the paperwork and the calls between appraisers, not in some final dramatic hearing.

When an umpire enters the picture

If the two appraisers can't agree, they select an umpire. The umpire is a neutral third party. That person reviews the evidence and helps break the impasse. In many policies, any agreement by two of the three decides the value and binds both sides.

This is why the quality of the written appraisal matters so much. By the time an umpire sees the file, unsupported complaints have very little value. Clear comps, accurate equipment matching, and a disciplined rebuttal carry the weight.

A simple view of the process looks like this:

| Stage | What happens | What you should do |

|---|---|---|

| Appraisers appointed | Each side selects its appraiser | Stay organized and responsive |

| Evidence exchanged | Reports, comps, and rebuttals are shared | Provide missing records quickly |

| Negotiation | Appraisers test each other's valuation | Let the evidence do the work |

| Umpire selection | Only if there's a deadlock | Review expected costs and timing |

| Binding decision | Two of the three agree on value | Confirm payment details in writing |

Costs and practical pressure points

Policy language often requires each side to pay its own appraiser, while umpire costs are commonly shared. The exact handling depends on the policy and the claim. Before the process gets too far, read the clause carefully and ask how the insurer interprets cost responsibility.

The practical headaches usually aren't legal. They're logistical.

- Storage fees: Don't ignore where the vehicle is sitting.

- Rental pressure: If you're in a temporary car, time matters.

- Loan payoff issues: A lender can add urgency even when the value is still disputed.

- Paperwork delays: Titles, powers of attorney, and lien documents can slow final payment.

What a fair ending usually looks like

A clean resolution isn't about “beating” the insurer. It's about forcing the file toward a supportable number. Sometimes the result comes through direct agreement between appraisers. Sometimes an umpire signs off after reviewing both sides. Either way, the strength of your case turns on preparation.

By the end, most owners see the process differently. The adjuster's first number felt absolute. The appraisal process shows it was just one position in a dispute that could be tested.

Taking Control of Your Total Loss Settlement

A total loss settlement dispute gets easier to manage once you stop treating it like a customer service problem. It's a contract problem and a valuation problem. That shift matters because customer service arguments go in circles. Contract rights and evidence create movement.

The pattern is usually the same. The insurer makes an offer based on a report. You review the report, document the errors, gather local support, and push for correction. If the adjuster won't move, the appraisal clause gives you a way to force the value question into a structured process.

That's the part too many drivers never hear clearly enough. You are not stuck with endless phone calls. You are not required to become a valuation expert overnight either. What you do need is a disciplined response, good records, and the willingness to use the procedure built into the policy when informal negotiation stops working.

The strongest position in a total loss claim comes from being organized early and decisive once the dispute becomes clearly about value.

If you're in Oregon or Washington, local market knowledge can make a real difference. So can having someone who knows how to read a CCC ONE or Mitchell report without taking its assumptions at face value. The first offer might be the start of the claim, but it doesn't have to be the end of the story.

If you want a second set of eyes on your claim, Leverage Auto Appraisals offers Oregon-based total loss appraisal and negotiation support for policyholders in Oregon and Washington, including claim review, appraisal-clause disputes, and direct work with the opposing appraiser.